Prophetic or Precarious?

Demography as Economic Destiny

The simple math behind demographic trends appeals to many investors who think the raw number of people holds the future of major economic trends. But there’s still plenty of uncertainty to keep things interesting. We explore.

Demography appeals to investors who crave certainty, which demographic math provides

Media stories are replete with demographic doomsaying. A shortage of workers. A lack of immigration. In some regions, there are too many people. In others, too few children. Aging and the burden of public sector costs. It goes on and on.

“Demographics” also serves as a catch-all excuse for many macro views. Some say interest rates will revert to pre-Covid levels in the developed world due to weak demand (“It’s demographics!”), while others worry about runaway inflation due to faster wage growth stemming from workforce shortages (“It’s demographics!”).

And surely you’ve heard the phrase, “Demography is destiny.”1 While we appreciate the catchy alliteration, demography appeals to investors who crave certainty, which demographic math provides (as we shall see below).

But we also think the “demographics” phrase gets thrown around too often with vague usage.2 To explore the topic, we’ll first act as if demographics drive everything and follow where the math leads. Then, we’ll point out possible deviations from such demographic determinism. Finally, we’ll include some demographics-based prophecies.

Suppose you, dear reader, live long enough (say, the next 63 years). In that case, you may experience something unseen in human history

Suppose you, dear reader, live long enough (say, the next 63 years). In that case, you may experience something unseen in human history for at least the last 60,000 years: the peak and prolonged decline in the size of the human population.

That’s right, not since humans migrated out of Africa millennia ago has the number of humans roaming the earth gone in reverse for any extended period. But by 2086, the human population could peak at around 10.4 billion and begin to decline.3

Why the decline? It won’t be because of climate change or a pandemic. Of all the supply chain problems consumers have faced, one product’s production process is difficult to change: human beings.

Despite scientific advances, producing human offspring still requires a 40-week gestation period—and then nearly two decades of care and comfort to create a fully functioning adult of use to society (or longer for some).

As such, for every two people choosing to produce offspring, only so many new children can appear in the decades ahead. To “replace” the current population, the fertility rate—the average number of children born to every woman—would need to be at least 2.1 (to account for more boys being born than girls). Once we know how many people we have now and how many new ones we can produce each year, we can guess how many people will exist in, say, 20 years.

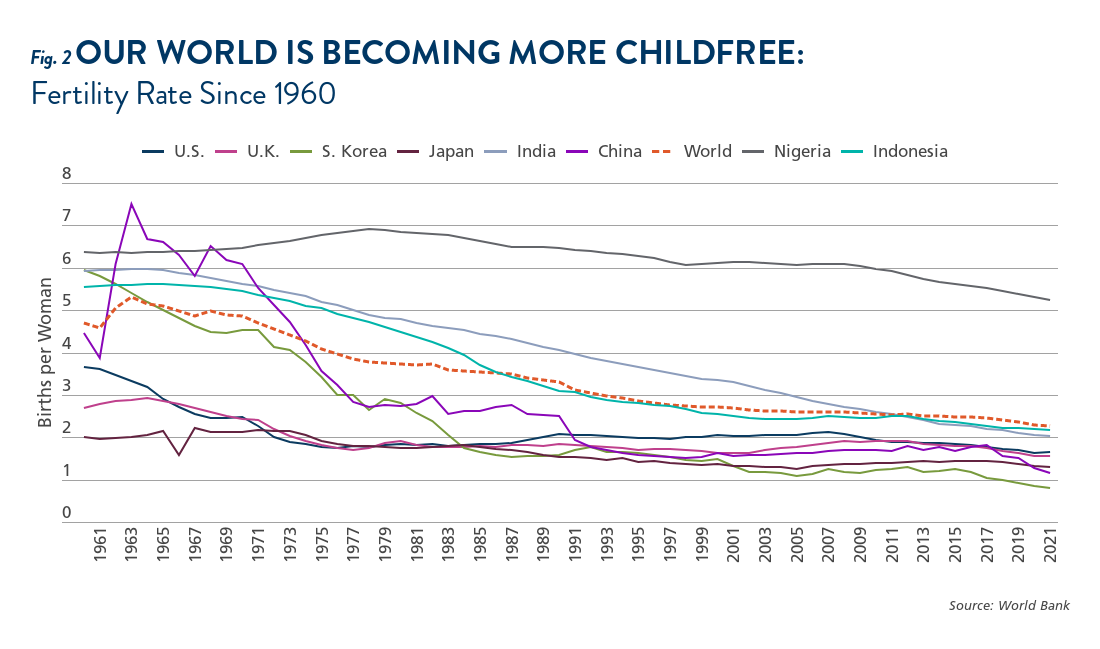

South Korea serves as the perfect example of declining birth rates. The South Korean fertility rate has dropped 86% since 1960, from almost six births per woman to 0.81 in 2021! According to the United Nations’ World Population Prospects report, South Korea’s population could fall by around 20 million in the next 50 years. That is despite the United Nations’ slightly higher fertility rate projections!

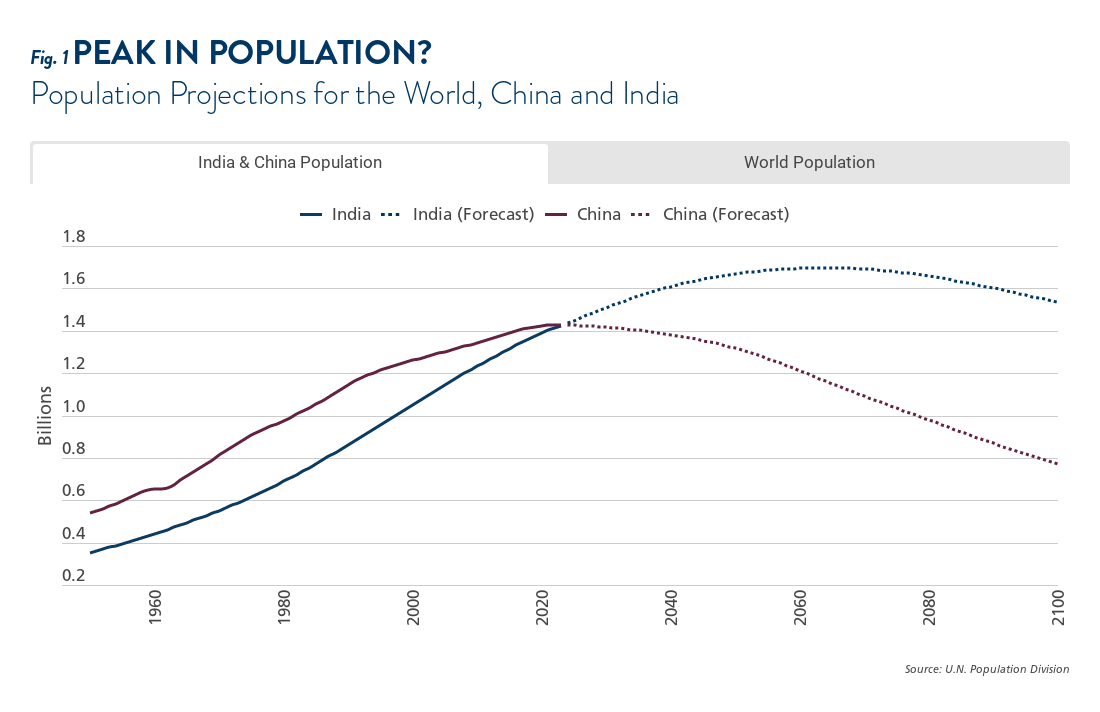

China, often the poster child for discussions of demographic doom, faces a similar predicament. China’s fertility rate is already down to 1.16 births per woman, so China’s population could decline by around 654 million in the decades ahead from the current tally of 1.4 billion.

The South Korean fertility rate has dropped 86% since 1960, from almost six births per woman to 0.81 in 2021!

Interestingly, India may fare best (at least if the goal is to have more people!). Based on current figures, the long-term population of India could reach 1.7 billion, around 600 million more than China’s at that point (see Figure 1). Imagine the geopolitical consequences.

However, India may fall well short of 1.7 billion people. India’s fertility rate is already at 2.0. And India’s overall fertility rate is 1.6 in urban areas, well below the replacement rate.4

Africa is the exception, but as per capita incomes rise, fertility rates usually fall, as seen elsewhere. Also, Africa will likely need more time to grow to offset shrinking populations elsewhere.

Overall, the total world fertility rate was 2.27 in 2021, according to the World Bank (see Figure 2). When will the world rate dip below the 2.1 threshold? Possibly as soon as the next two decades.

With the math outlined, as the cool kids say, “Numbers don’t lie.”

But now we examine the gray areas.

First, fertility rates could pick up, whether through government incentives, cultural shifts, or technological advances—nothing is inevitable.

Some readers may wonder, what about immigration? Unfortunately, immigration means moving humans across different borders on the same planet. Since, on a net basis, the Earth still likely faces population decline, individual regions may gain residents only due to the loss of residents from elsewhere.

Moreover, many of our readers may rejoice over the population news (and some may even argue it could not happen soon enough!). Fewer people equals less demand for natural resources. Better for the environment, the story goes.

Unfortunately, this story, though popular, is wildly short-sighted.

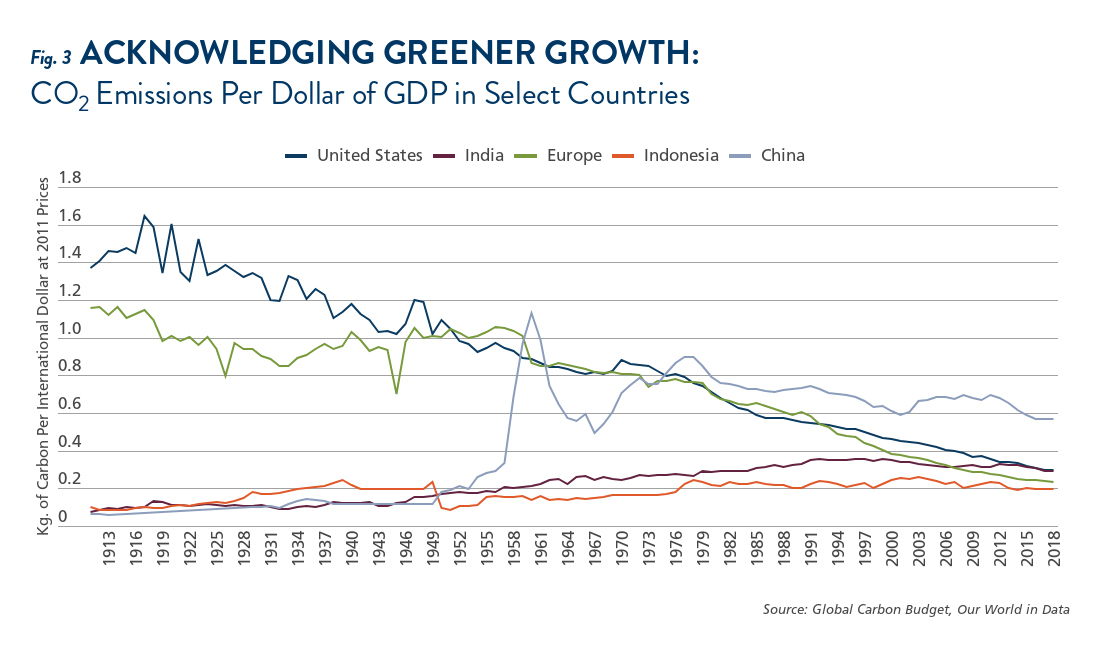

First, global economies have already become less resource-intensive over the last few decades, even as the population reached new global heights (see Figure 3).

Second, at first blush, fewer people mean slower economic growth if productivity growth rates remain similar to historical norms. After all, economic growth is simply the number of people working and the output they produce over time—productivity. In the U.S., for example, labor productivity averaged ~2% in the 50 years pre-Covid. With a 1% workforce population growth, overall economic growth trended at ~3% annually. However, even with average productivity growth, overall GDP will struggle to expand if population growth goes negative.

A critical problem with a lack of economic growth is ballooning government debt. The only way to overcome a debt problem is to be ever more productive to offset population decline. Otherwise, the demographic burden will become a hefty fiscal burden, especially if public health and pension costs also grow as aging occurs.

Could productivity growth pick up to offset demographic decline? Advances in machine learning (see our centerpiece on this issue) provide some hope that technological advances could push productivity upward, but the math is difficult to overcome. That said, there is hope: since the 1950s, only about 15% (or 0.3 percentage points) of U.S. economic growth is due to population growth.5 Rising educational attainment, more research & development, and a rising share of the population working contributed more to growth.

In addition to the debt issue, a shrinking labor force may imply higher inflation and interest rates. When viewed on a longer-term time scale, interest rates have been low and declining in the developed world since the mid-to-late 1980s. Inflation had also been quiescent. What else occurred during that era? A massive positive labor supply shock with the inclusion of China and Eastern Europe back into the world economy.

Economists Charles Goodhart and Miraj Pradhan note that “the integration of China into the global manufacturing complex by itself more than doubled the available labour supply for the production of tradeable products among the advanced economies.”

They write, “The increase in the working-age population (aged 15–64) in China outstripped the combined increase in Europe and the USA from 1990 to 2017 over fourfold.” China injected over 240 million workers into the global working-age population, while the U.S. and Europe chipped in “less than 60 million.”

The collapse of the USSR also brought “the whole of Eastern Europe, from the Baltic States, through Poland down to Bulgaria,” into the world’s trading system, an increase of roughly 210 million people.

Combined, the rise of China and the return of Eastern Europe into the world trading system “produced the largest ever, massive positive labour supply shock.”6

As a result of the labor flood, globalization flourished, with trade growing by 5.6% per year from 1990 to 2017, outpacing world GDP growth of 2.8%. China deserves the bulk of the credit. In 2004, its share of world manufacturing output was 8.7%. By 2017, it had surged to 26.6%. In turn, worldwide consumers enjoyed cheaper goods, and corporations basked in record corporate profits generated using cheaper labor.

Of course, inquiring minds must ask the looming question: What happens when a positive labor shock turns negative? Could we be in for more inflation and higher rates? It’s worth considering that things have changed, and no such demographic flood awaits in the wings.

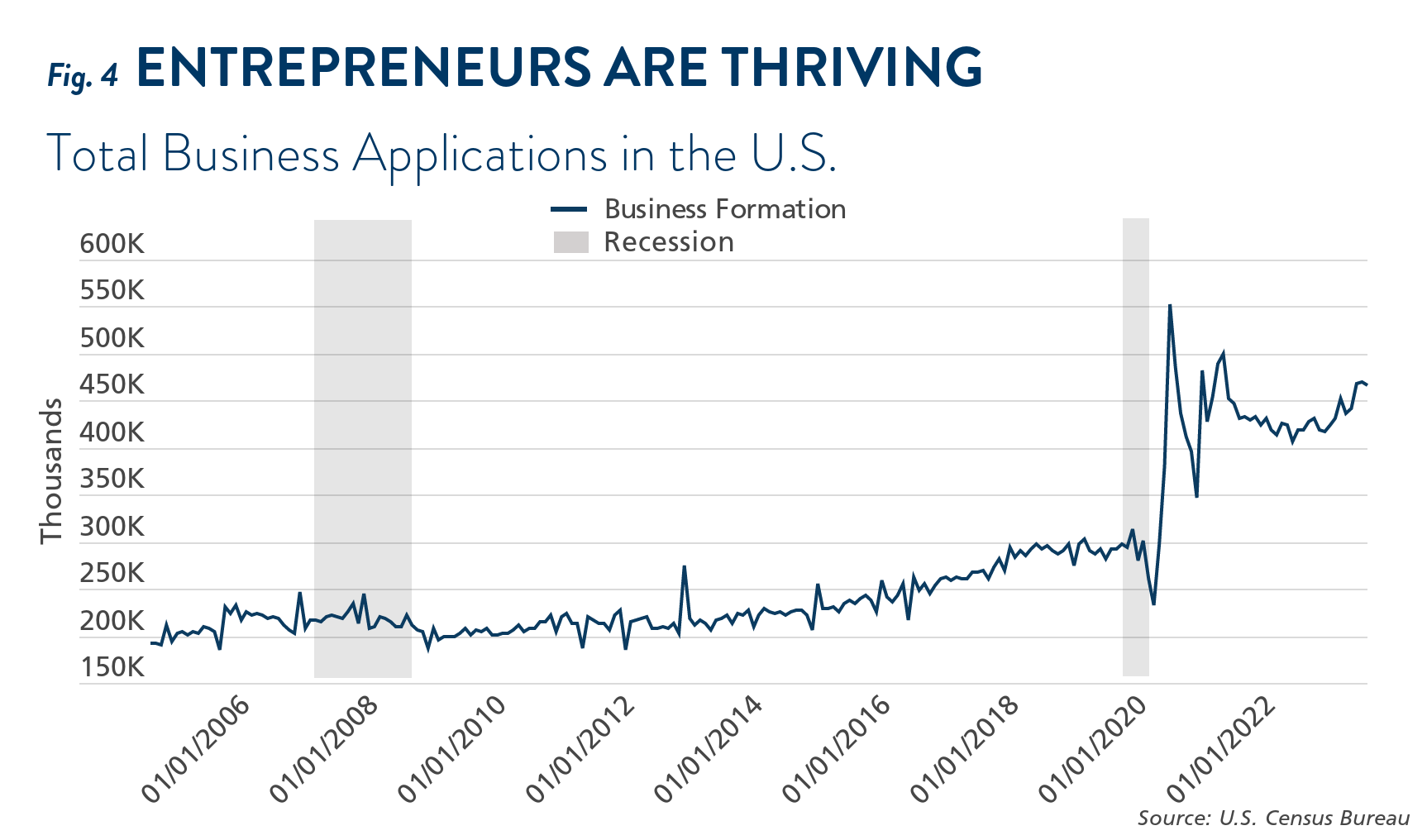

For us, the biggest problem of population decline is that fewer people will generate fewer ideas. Some research indicates that ideas are becoming more difficult to find, and most growth comes from new firms forming (based on new ideas). Fortunately, at least in the U.S., new firm formation appears to be trending up (see Figure 4).7 But we wonder whether this will persist with aging populations and shrinking labor forces.

In addition, we can also posit some other societal impacts in the decades to come from fewer people roaming the planet. (Let’s call them what they are: more prophecies than prognostications.)

First, aging populations combined with fewer children per adult is an utterly unique and fascinating social phenomenon. In places where we see one-child families with both living grandparents and two adults raising and nurturing the child—the youth have never enjoyed such a focus of societal attention!

Second, college enrollment may decline in the coming decades. Fewer children mean fewer students, fewer graduates mean fewer professors, and fewer professors probably mean fewer colleges. As for the institutions themselves, the stronger names and brands will survive, but fewer students will be left for the lower-tier institutions. We already see evidence of this in South Korea, where total student enrollment has declined for 18 straight years.8

Third, we’ll see a departure from certain countries, states, and cities. As population growth slows and society ages, migration patterns will increasingly move toward warmer climes, particularly in the American South and West. Still, one can think of other regions on Earth as well. Case in point: Maine managed just 12,006 births in 2021—based on our math above, we can expect a shrinking Maine population soon. As a consequence, house prices could fall in some locales. Will an aging population want to spend winter in the U.S. Northeast? Migration patterns could send prices tumbling and likely mean more bulldozers (for demolition instead of construction) in other regions.

Even a subject as seemingly simple as demographics, with some hard-to-argue-with math at its core, leaves ample room for uncertainty about the future, especially as we stretch into the next few decades, not just the next few years.

Nothing is predestined, but we hope this quick tour of the demographic landscape elucidates the problems and possibilities we may face.

Endnotes

1. Originally attributed to Auguste Comte2. Timescale is also essential. For those touting demographics as the primary reason for many near-term issues (e.g., inflation in 2021-23!), we doubt the story holds much water as the global population may peak in the coming decades but hasn’t yet in 2023.3. U.N. Department of Economic and Social Affairs, Population Division (2022). World Population Prospects 2022: Summary of Results.4. Ministry of Family Health And Welfare, National Family Health Survey - Fact Sheet (2021). International Institute for Population Sciences. http://rchiips.org/nfhs/factsheet_NFHS-5.shtml. 5. Jones, Charles I. (2023). The Outlook for Long-Term Economic Growth. Jackson Hole Symposium. 6. Goodhart, C., & Pradhan, M. (2020). The great demographic reversal: ageing societies, waning inequality, and an inflation revival. Palgrave Macmillan. 7. U.S. Bureau of Labor Statistics. (2023, July 26). Table 8. Private sector establishment births and deaths, seasonally adjusted. 8. Yoon, Dasle and Timothy W. Martin (2023, August 31). World’s Lowest Birthrate Sinks Further Despite Cash Payouts to Parents. Wall Street Journal.