IN GOOD

SPIRITS:

WHERE THE

"FAIR VALUE"

FOR THE 10-YEAR YIELD SHAKES OUT...WITH A TWIST

Investors often want a clear signal for when something is “cheap,” “rich,” or “fairly valued.” Nowhere is that more relevant than today in the fixed-income markets. With interest rates near multi-decade highs, investors want to be comforted that now is the right time to

buy. But is it?

If you’ve wondered about the “perfect recipe” for an Old-Fashioned cocktail, we have the answer: two ounces of Kentucky bourbon, a teaspoon of Demerara syrup, and a couple of dashes of Angostura bitters.

As a bond investor, you might also wonder, “What’s the perfect recipe for the fair value of a 10-year Treasury yield?” The U.S. 10-year Treasury yield is one of the most important interest rates in the world. It affects everything from mortgage rates to stock prices. The 10-year yield trajectory has perplexed investors lately, as it started 2023 at 3.87%, fell to 3.31%, and then surged to 4.99% in the fall before it ended the year at 3.87%. As of this writing, the 10-year is hovering around 4.50%.

As a bond investor, you might also wonder, “What’s the perfect recipe for the fair value of a 10-year Treasury yield?”

Like equity investors with their target “S&P 500 level,” bond investors seek the bond market’s holy grail: the “fair value” of the 10-year Treasury note yield.

Fortunately, we have a “recipe” for the fair value of the 10-year yield—or at least a framework for thinking about longer-term yields. By looking at history and economic variables, we can get a sense of what the fair value of the 10-year yield might be. For example, at a yield of 0.90% in August 2020, 10-year Treasury notes were far too rich (remember, prices and yields are inversely related). However, by the fall of 2023, perhaps Treasury notes were more fairly valued instead of too cheap.

Below, we’ll explore the three primary ingredients in the 10-year fair value recipe: the inflation premium, the concept of “real rates,” and the term premium. Once you understand the ingredients, you can mix your own cocktail.

AVOIDING EROSION

In building our fair value for the 10-year yield, we were inspired by a framework from former Fed Chair Ben Bernanke, who stated that “it is useful to decompose longer-term yields into three components” that include “expected inflation over the term of the security; another capturing the expected path of short-term real, or inflation-adjusted, interest rates; and a residual component known as the term premium.”1

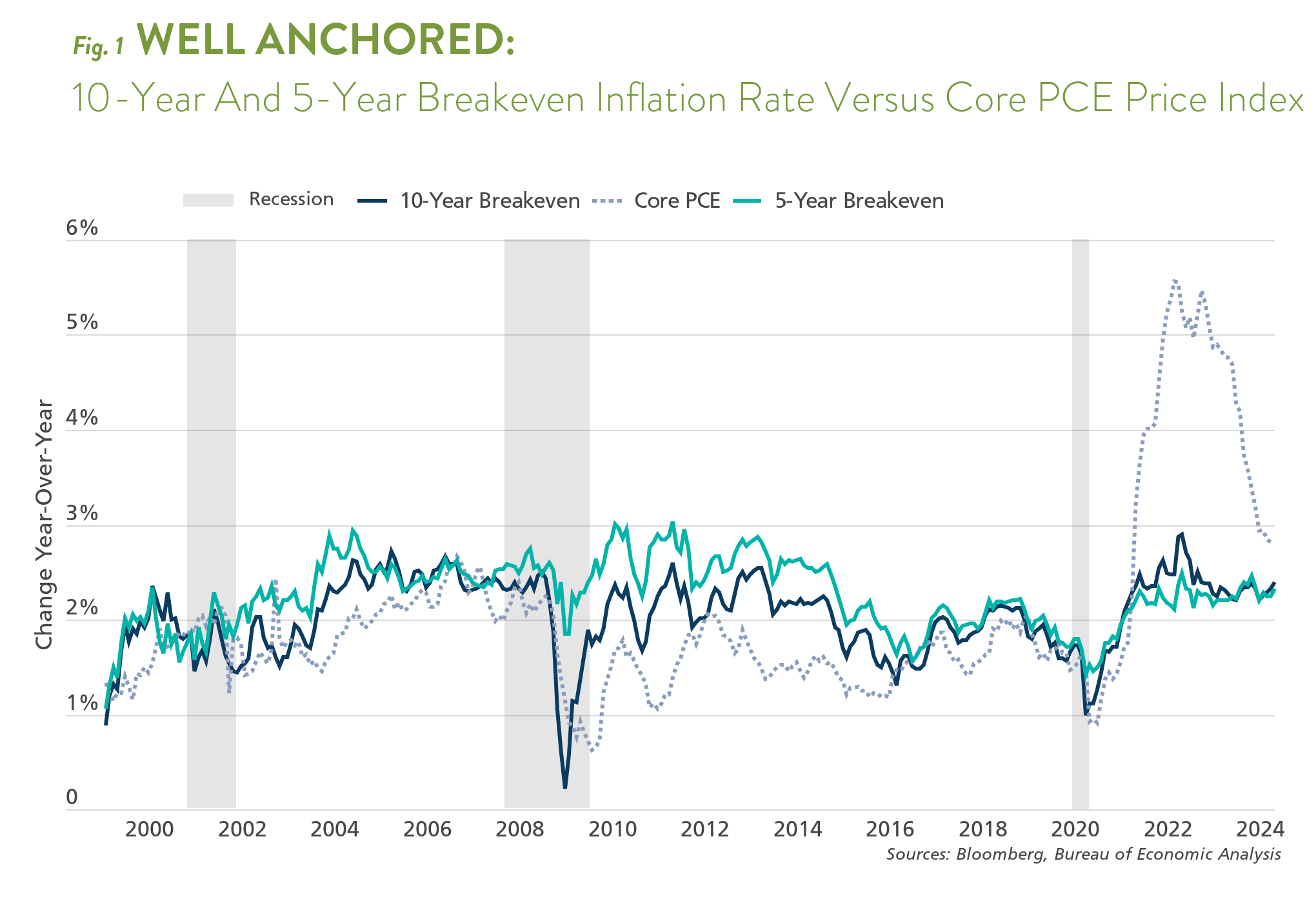

A common way to gauge the market’s expectations for inflation is to look at the 10-year breakeven inflation rate. The breakeven rate is calculated by looking at the difference in yields of Treasury Inflation-Protected Securities (TIPS) and nominal Treasury bonds of the same maturity, thereby extrapolating current inflation expectations.

Despite actual inflation rising sharply between 2021 and 2023, the breakeven inflation rate increased to 2.9% before retreating to 2.3% (see Figure 1). Inflation expectations remain, as the central bankers say, “well anchored,” as investors trust inflation will return close to 2% over time.

But what will inflation average for the next 10 years? Many investors believe (hope?) that inflation will revert to the pre-Covid “norm.”

Given that the median age of an investment analyst is 40, a return to low inflation is an all-too-obvious guess. After all, the median financial analyst has only been of working age for less than two decades, when the average 10-year breakeven inflation rate was 2%!

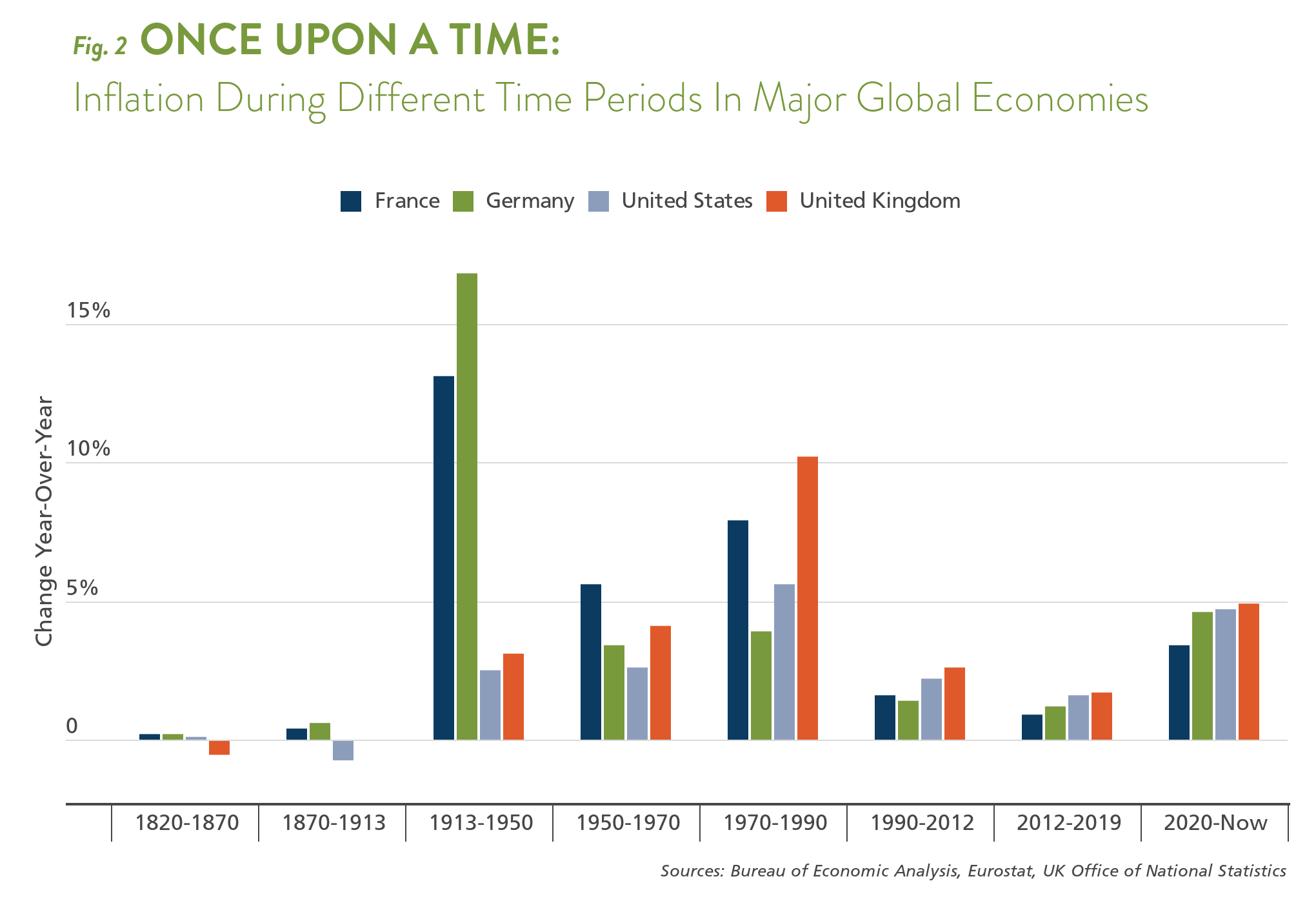

So, before pouring that 2% into your glass, remember that before 2000, global long-term inflation figures were much higher, averaging close to 6% in the U.S. and 10% in the UK (see Figure 2)! Taking a broader view, it becomes evident that the most recent three decades might be outliers in macroeconomic history, not just in the U.S. but globally.

Why might inflation remain higher in the post-Covid era than during the prior two decades?

Once elevated, inflation has historically taken time to recede, and there are often bumps along the way

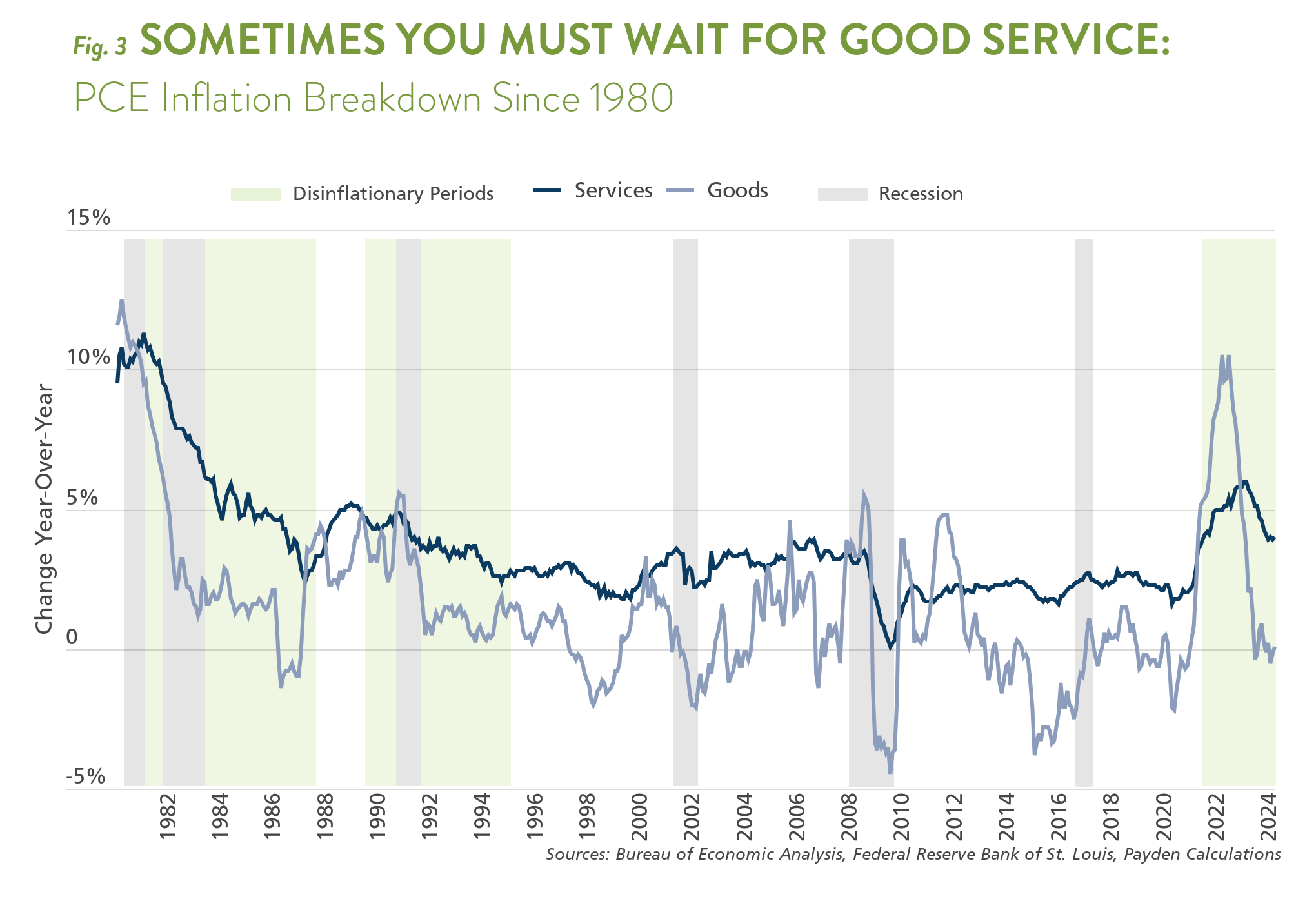

First, once elevated, inflation has historically taken time to recede, and there are often bumps along the way. After all, the U.S. economy has faced only three disinflationary periods (when inflation slowed but remained positive), during which we witnessed a significant decline in inflation. These periods began in 1980, 1989, and July 2021 (currently underway). The two prior episodes required between five and seven years (including a few recessions) to see inflation subside finally.

One reason for the slow progress on inflation is that while goods prices fell quickly in the abovementioned periods, “the last mile of disinflation is driven primarily by a lengthier disinflation of services.”2 In the current episode, goods prices have dropped quickly as supply chains have returned to normal, but service prices are taking much longer to subside. After all, as of this writing, we are just coming off a quarter where progress on inflation has been halted primarily due to a pick-up in the prices of services (see Figure 3).

Second, the Covid era's fiscal and monetary policy mix was incredibly potent, threatening price stability. However, while inflation erupted, the labor market healed quickly from the Covid downturn. As a result, some policymakers focused on employment may see the current era as evidence of a better policy mix than the stagnant growth years of the 2010s, leading them to tolerate (or even foster) more inflation in the decade ahead than in the prior 20 years.

Suffice it to say that, as investors, it is prudent to plan for a bit higher inflation in the coming decade than in the past. Much like we would prefer a finely aged 10-year barrel-strength bourbon, for now, we’re assuming 2.5% inflation over the next 10 years (versus 1.6% in the 2010s) and pouring that variable in first to our fair value model. Now, onto the next ingredient.

KEEPING IT REAL

The next part of the recipe is the path of real (inflation-adjusted) interest rates over time. One way to conceptualize the real interest rate over time is to consider the fed funds rate path. Why? Because longer-term interest rates are a collection of short-term interest rates.

But, in the short run, the expected path of short-term interest rates can vary considerably. Monetary policy influences this path—both the actual policy stance (i.e., today’s federal funds rate) and market participants’ expectations of how policy will evolve (forward guidance or “jawboning”).

Longer-term interest rates are a collection of short-term interest rates.

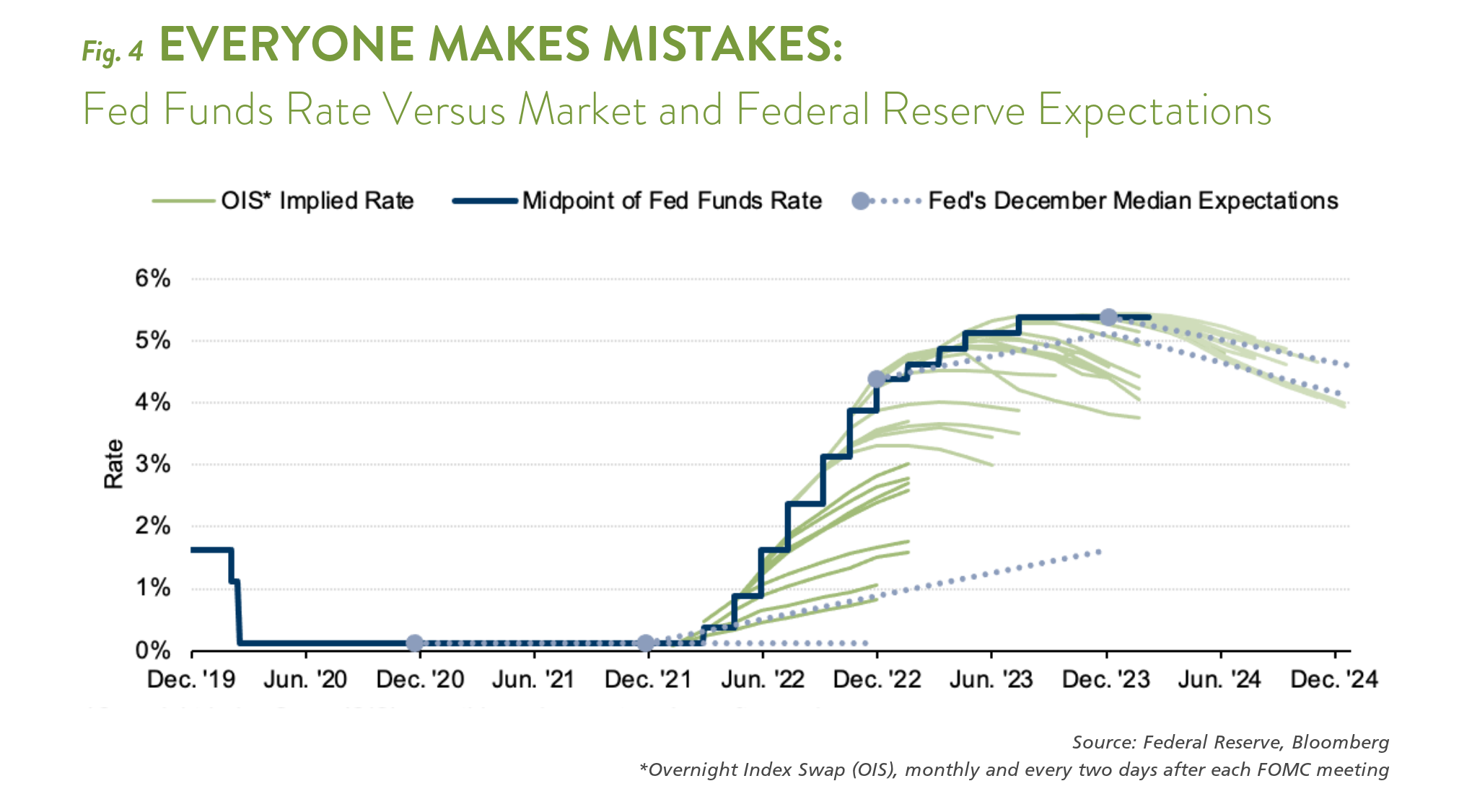

To estimate the short-term rate trajectory, like the inflation premium, you could take the market’s implied “forecast” for the nominal fed funds rate path as the starting point for this second ingredient. However, doing so would be about as boring as using generic simple syrup, and as we show in Figure 4, it often tastes odd (read: wrong).

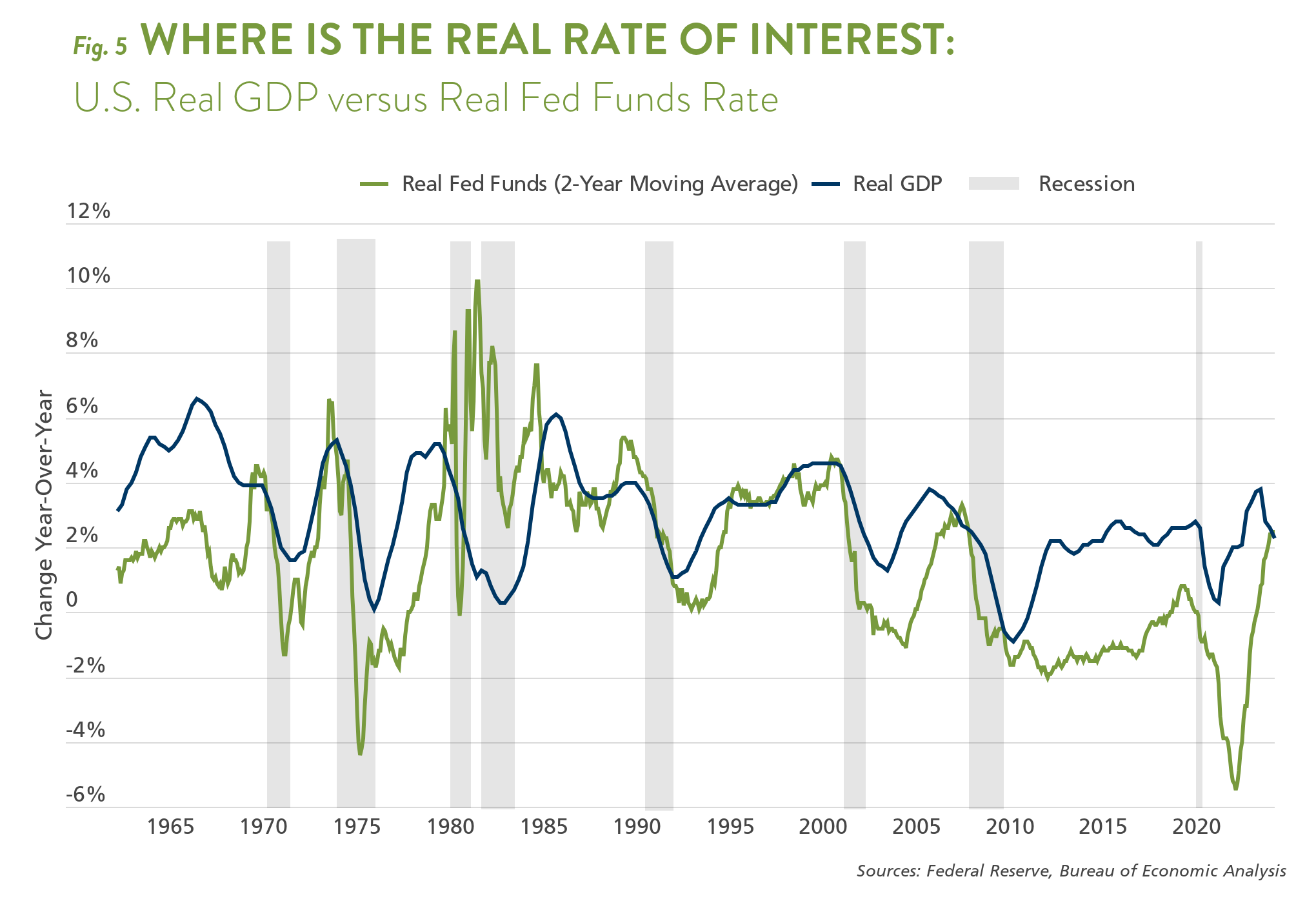

However, central bankers can only influence nominal rates in the short run—the dirty secret of monetary policy and longer-term interest rates. Over the long run, say the next 10 years, non-monetary factors such as expected return on investment driven by expected real economic growth are primary drivers of changes in real interest rates (see Figure 5).

Why was the real rate so low in the 2010s? Low and negative short-term rates, which prevailed for the better part of the 2010s, reflected sluggish economic growth and too much pessimism about future economic output and investment returns. This extreme pessimism may be lifting, which is a good sign for the economy.

Why could real output be higher in the 2020s than in the 2010s? Increased labor is a possibility, as more aggregate hours worked means stronger output growth. In the 2010s, the labor force grew at an average annual rate of 0.7%. The 2020s could be different, as the average growth rate of the labor force over the last three years has been higher at 1.4%.3

In addition to labor force growth, productivity growth is the other key element of output growth. Productivity is how much a worker produces for each hour worked. Indeed, over the past 12 months, productivity, or output per labor hour, has increased by 2.9%. Productivity growth averaged just 1.3% in the 2010s. Will the recent pick-up be sustained?

It’s possible. Kahn and Rich (2007) analyzed labor productivity in the post-war period in the U.S. They found that the economy has switched between four high (~3.0%) and low (~1.3%) productivity growth regimes.4 The most recent time we enjoyed a high productivity growth regime was from 1997 to 2005—after 25 years in a low-growth one.

Research also shows that the real limiting factor for output growth is not capital or labor but new ideas. We are nowhere close to “run[ning] out of people to hunt for new ideas” as the “pool from which we may find new talented inventors will multiply.”5 The dawn of the era of large language models (e.g., ChatGPT) might usher in greater productivity as the ability to search for and test new ideas increases with the proliferation of artificial intelligence (AI) tools.

Because real output is the product of the number of people employed in the labor force and their productivity, a period in which output grows above 2% in real terms, and not 1.5%–2.0%, remains possible. In turn, we suspect the real interest rate component of our 10-year fair value recipe could be higher than that which prevailed over the preceding decade. How high is anyone’s guess, but real rates were closer to 4% in the productivity-fueled growth era in the late 1990s.

Suppose we return to a period similar to the 1990s with real rates around 2.7% (the average recorded from 1990-1999). A 2.0% rate for our fair value cocktail might be a fair bet, and we will update the recipe to taste over time.

Congratulations, we have our simple syrup. However, as much as you could choose pure cane sugar, granulated brown sugar, or even maple syrup for your cocktail, you have to determine the best way to chart the forward path of short-term real rates. Even our choice of demerara sugar could be light brown, dark brown, or even golden in color. Ultimately, it will all depend on your taste—and the evolution of macroeconomic data.

THE SECRET INGREDIENT

The last ingredient in an Old Fashioned cocktail is a few dashes of Angostura bitters. No one knows the exact recipe for Angostura bitters, but every bartender adds a non-scientific “dash” or two of bitters to a glass. The term premium in our fair-value cocktail is not much different from the “secret ingredient.” The Wall Street Journal even published an article: “Wall Street’s Latest Obsession Is an Unknowable Number.”6

Simply put, after being compensated for inflation and the short-term rate of interest one could earn, investors often want additional compensation for having their capital locked away for 10 years. After all, with the debt ceiling showdown and a global pandemic fresh on our minds, a lot can change in the next 10 years.

We think it’s prudent to factor in a higher term premium than experienced in prior periods

Since the term premium is unobservable, economists have used financial and macroeconomic variables to estimate it. One of the most prominent models hosted on the New York Federal Reserve’s website—the Adrian, Crump, and Moench 10-year Term Premium—rose to the highest levels since 2015 to 0.34% in October 2023 (see Figure 6).7

Regardless of your estimate, the term premium has likely risen again (see Figure 6 again). What could foster uncertainty in the coming decade and prevent the term premium from dipping below zero anytime soon?

Perhaps most worrying, the U.S. Treasury admits it will likely need to borrow a net $6.3 trillion from the public over the next three years. For context, in 2009, the entire stock of marketable Treasury debt outstanding was just $6.3 trillion.8 Fiscal issues of this magnitude were absent in the 1990s and the 2010s. As a result, we think it’s prudent to factor in a higher term premium than experienced in prior periods. We will be generous and pick 0.5%, roughly in the middle of the various model estimates.

Now that we have our three ingredients, stir and add the orange peel garnish.

POUR IT ON THE ROCKS, STIR, AND ENJOY

Before you pour yourself an Old Fashioned to celebrate this achievement, remember that even if you follow our proportions and recipes, your cocktail will only be as good as the quality of your ingredients. A fair value calculation is no different. That said, we think investors ought to be a) compensated for inflation and inflation risks, b) rewarded for the economy’s real output growth, and c) compensated for other risks.

Let's assume inflation averages a higher rate (2.5%) in the next ten years than in the previous decade, a higher real rate (2.0%), and a wider term premium (0.5%). Where does that leave us with “fair value”? Using the historical relationship between these three ingredients and the 10-year yield in the past, our “spec,” as bartenders say, will put us at a fair value of 4.7%–5.1%.9

No one can forecast the future with certainty. But by looking at history and economic variables, we hope we have given you a better framework

If you have a different interpretation, that’s fine! Just let us know if you changed one, two, or all our ingredients. Everyone has their own personal tastes in cocktails. Further, you might wonder whether the above exercise helps investors ponder global interest rates—it does, because global yields tend to move in sympathy with longer-term U.S. rates (see Did You Know? Box - One World, One Rate).

No one can forecast the future with certainty. But by looking at history and economic variables, we hope we have given you a better framework for assessing the fair value of the 10-year yield. While longer-term rates are more fairly valued, depending on your outlook, it might not be quite right to call them “cheap.”

Either way, we hope you find your ingredients and enjoy your Old Fashioned.

While we spent time discussing the fair value of the 10-year U.S. Treasury yield, we know that the 10-year government bond yields of the U.S., Germany, France, and the United Kingdom are correlated with each other with an R2 (strength of the relationship) of 0.8-0.95 based on monthly data of 10-year debt issued since 1960 (see Figure 7). Good news! Unlike an Old Fashioned, your conclusions on long-term interest rates should be the same, regardless of whether you pour in bourbon, gin, brandy, or a Jägermeister! How convenient!

Endnotes

1. Bernanke, B. (2013, March 01). Long-Term Interest Rates [Conference Session]. Federal Reserve Bank of San Francisco. https://www.federalreserve.gov/newsevents/speech/bernanke20130301a.htm

2. Gascon, Charles S. and J. Martorana. (2024, April). Historical Disinflation Episodes: Which Falls First, Goods or Services? Federal Reserve Bank of St. Louis. https://research.stlouisfed.org/publications/economic-synopses/2024/04/17/historical-disinflation-episodes-which-falls-first-goods-or-services#:~:text=Historical%20experience%E2%80%94specifically%2C %20disinflationary%20episodes,a%20lengthier%20disinflation%20of%20services.

3. In Chair Powell explained at the May FOMC press conference that the recent increase in the labor force “reflect[s] increases in participation among individuals aged 25 to 54 years and a continued strong pace of immigration.” In fact, according to the CBO’s latest demographic update, net immigration could have been 3.3 million higher than expected in 2022 and 2023. https://www.cbo.gov/system/files/2024-01/59697-Demographic-Outlook.pdf

4. Kahn, J. A., & Rich, R. W. (2007). Tracking the new economy: Using growth theory to detect changes in trend productivity. Journal of Monetary Economics, 54(6), 1670–1701. https://doi.org/10.1016/j.jmoneco.2006.07.008

5. Jones, C. (August 2021). The Past and Future of Economic Growth: A Semi-Endogenous Perspective (Working Paper No. 29126). National Bureau of Economic Research. https://www.nber.org/papers/w29126

6. Goldfarb, S. (2023, October 18). Wall Street’s Latest Obsession Is an Unknowable Number. Wall Street Journal. https://www.wsj.com/finance/investing/wall-streets-latest-obsession-is-an-unknowable-number-f67248de

7. Treasury Term Premia, Federal Reserve Bank of New York. https://www.newyorkfed.org/research/data_indicators/term-premia-tabs#/overview

8. Office of Debt Management. (August 2022). Treasury Presentation to TBAC-Fiscal Year 2024 Q2 Report. U.S. Treasury Department. https://home.treasury.gov/system/files/221/TreasuryPresentationToTBACQ32022.pdf