THAT 90'S SHOW:

CAN THE REMAKE LIVE UP TO THE ORIGINAL

Boy band reunions, baggy jeans, and not-so-smart phones—nostalgia for the 1990s is rising. We apply this trend to consider possible paths for the economy in the 2020s.

A popular American television series, That 70s Show, debuted in 1998 and chronicled the lives of teenagers during the 1970s. The sitcom appealed to those coming of age after the 1970s who “missed out” on disco music, the parties, and the ample use of polyester in apparel. For those who lived through the 70s, the show served up a healthy dose of nostalgia. Now, 25 years later, a spin-off show focusing on the 1990s, That 90s Show, has debuted.

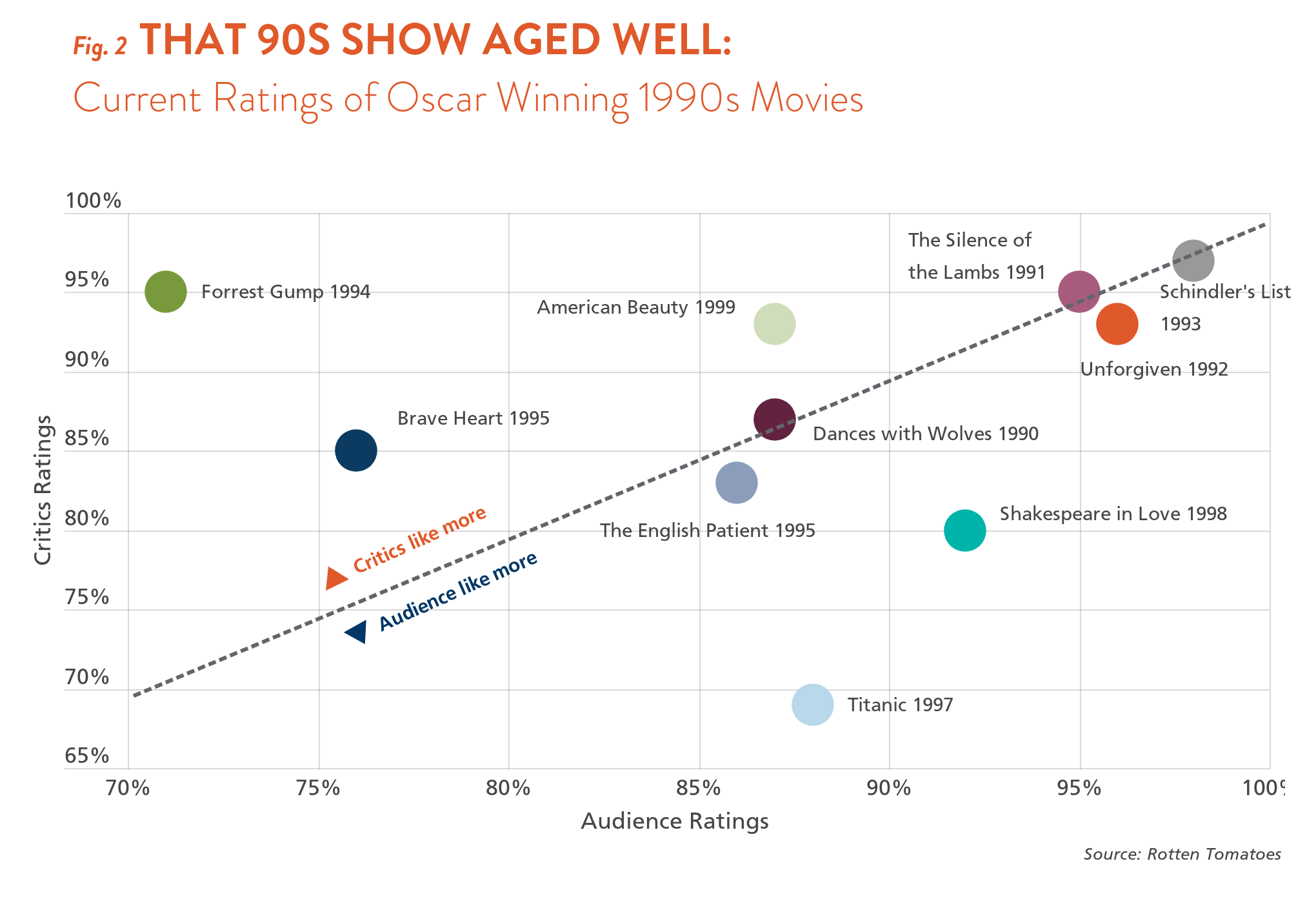

The timing is apt, as many of us who lived through the 1990s remember it fondly. The Soviet Union unraveled in the early 1990s, leaving America as the lone global superpower. The dawn of the internet brought seemingly endless possibilities, and a slew of new companies were born (The “Dot Coms”). Grunge music, hip hop, boy bands, Total Request Live, Titanic, Friends, and Seinfeld dominated the cultural consciousness (see Figures 1 and 2).

The 1990s also featured minimal movements in the fed funds rate, and a productivity boom engendered an extended period of economic growth, low inflation, and falling unemployment. We probably didn’t appreciate the 1990s as much as we should have, at least from an economic perspective. As such, we’ll detail the key features of how the decade unfolded and then ask if history could repeat.

FALL OF THE WALL

Unofficially, the 1990s kicked off on November 9, 1989. That was the day the Berlin Wall unexpectedly began to crumble, shocking the world and marking the beginning of the end of the Soviet “Iron Curtain” looming over Europe. The dissolution of the Soviet Union also left a global geopolitical power vacuum: the United States was, militarily at least, unrivaled—the world was suddenly unipolar.

Unofficially, the 1990s kicked off on November 9, 1989. That was the day the Berlin Wall unexpectedly began to crumble

The fall of the wall also meant millions of East Germans united with the West. Sure, reunification was costly, with Germany lagging in economic growth in the 1990s, but Europe fared well overall. In 1992, the Maastricht Treaty birthed the European Union, and in 1999, the euro and the European Central Bank (now 25 years “young”!) were launched.

The U.S. quickly squashed geopolitical spats. When Iraq invaded Kuwait in August 1990, the confrontation between the two largest petroleum-producing countries sent oil prices up 83% within two months and triggered a mild U.S. recession. However, the overwhelming U.S.-led coalition forces quickly drove Iraq back. The war's swift end allowed Kuwait to resume its oil production quickly. Consequently, oil prices receded to near their decade-low levels.

THE RISE OF CHINA

Overall, the global economy absorbed hundreds of millions of workers formerly cordoned off from the world before the 1990s. Like the reunification of Europe, millions of agricultural workers in China’s countryside flooded into urban factories as China began its ascent on the world scene as a trading and exporting nation. The redistribution of “floating populations” in new sectors increased labor productivity in China and fueled the nation’s position as the world’s largest exporter in the following decades.

As the 1990s began, U.S. exports were $515 billion while imports were $598 billion, leaving a trade deficit of $83 billion. By the decade's end, the trade deficit had tripled to $302 billion, while China’s trade surplus more than doubled. Although politically unpopular, the increase in trade “released pressure from rapidly growing domestic demand, pressure that would otherwise have shown up as higher inflation and interest rates.”1

“IT’S THE ECONOMY, STUPID.”

The 1990s also brought the rise of the baby boomers as a political group, with William Jefferson Clinton (born 1946) sworn in as U.S. President in January 1993. Clinton personified a trend in the Western world toward embracing markets. Specifically, “Clintonomics [tried to] adopt some of the pro-market orientation associated with the ascendancy of the Republicans in the 1980s, and marry it with traditional Democratic values such as concern for the environment and a more progressive income distribution.”2 Or put simply by Clinton advisor James Carville, “it’s the economy, stupid.”

Indeed, pro-market Clintonomics achieved a significant milestone by the decade's end. With progressive tax bills and spending cuts under Clinton (although Congressman Newt Gingrich initially brought some reforms), the U.S. fiscal deficit turned into a surplus from 1998 to 2001, the first (and last!) time since 1981.

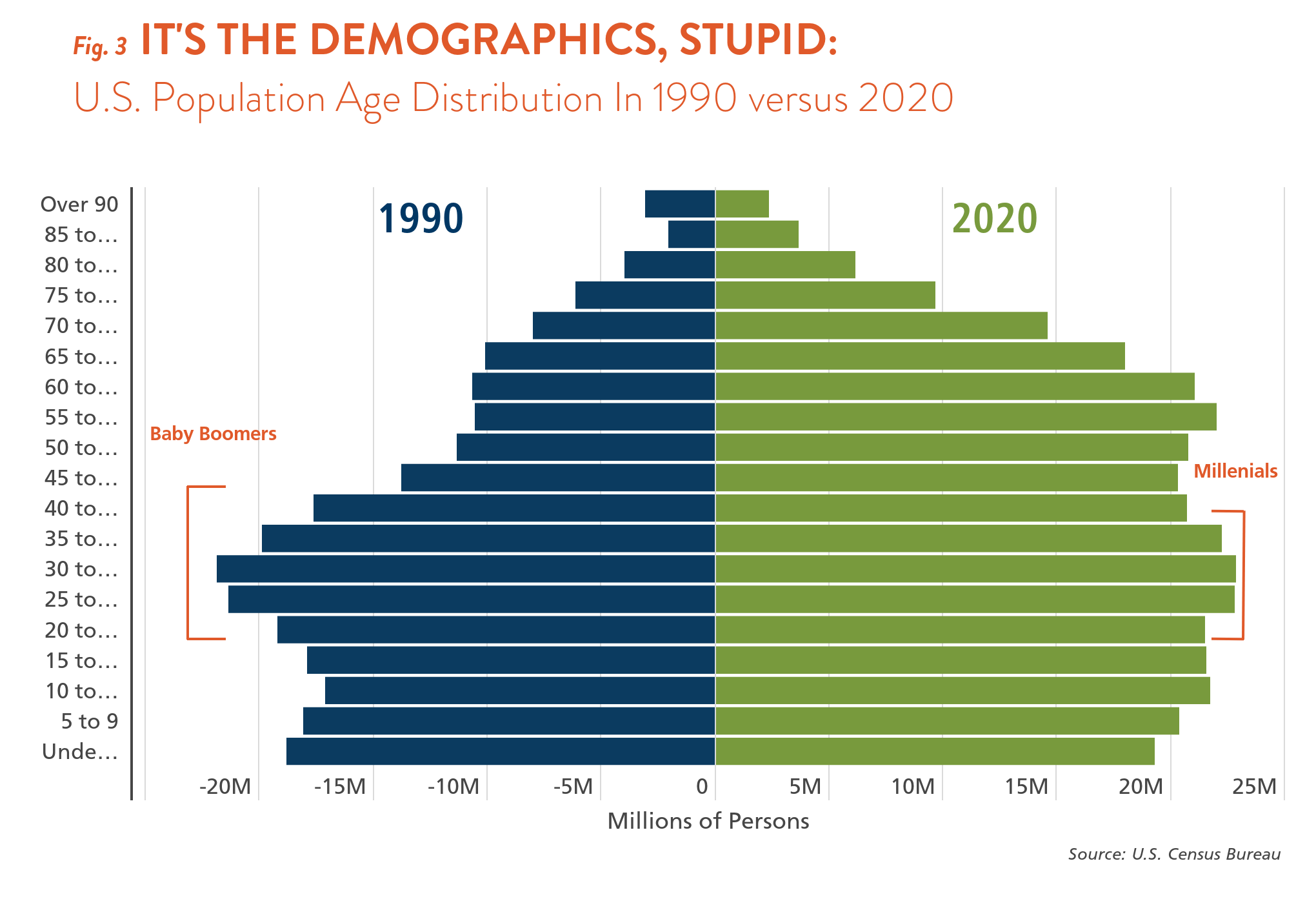

Moreover, in 1990, the youngest Baby Boomers turned 26—entering their prime age as workers and consumers. By 1999, the Baby Boomer population became the largest adult population cohort in the U.S. at 76.6 million and remained there until 2019 (see Figure 3).3 During the prime age of Baby Boomers, median household real income grew a cumulative 40% from 1993 to 2000. Consequently, consumer spending and fixed business investment increased 6% and 8%, respectively, on average annually during the 1990s, compared to 2% and 4% in the following two decades.

So, to put it another way—it’s also the demographics, stupid.

IRRATIONAL EXUBERANCE

As the economy boomed, markets melted up. In 1996, the notoriously obscure Fed Chair Alan Greenspan (he once remarked, “If I seem unduly clear to you, you must have misunderstood what I said.”4) was uncharacteristically clear about his take on the then-booming stock market, chalking up the share price surge to “irrational exuberance.”5

Indeed, a stock market boom powered by the rise of the “dot-com” companies characterized the late 1990s. Home computers' widespread affordability, popularity, and favorable capital policies allowed thousands of internet start-ups to flourish. Investment banks and venture capitalists flooding capital into them also fueled the rise of tech start-ups.

A stock market boom powered by the rise of the “dot-com” companies characterized the late 1990s

According to the National Venture Capital Association, annual venture capital investments increased from just $7 billion in 1994 to over $100 billion at the turn of the century. To put that in perspective, in recent times, annual venture capital raised averaged $35 billion in the following years until 2021, with $169.2 billion raised.6

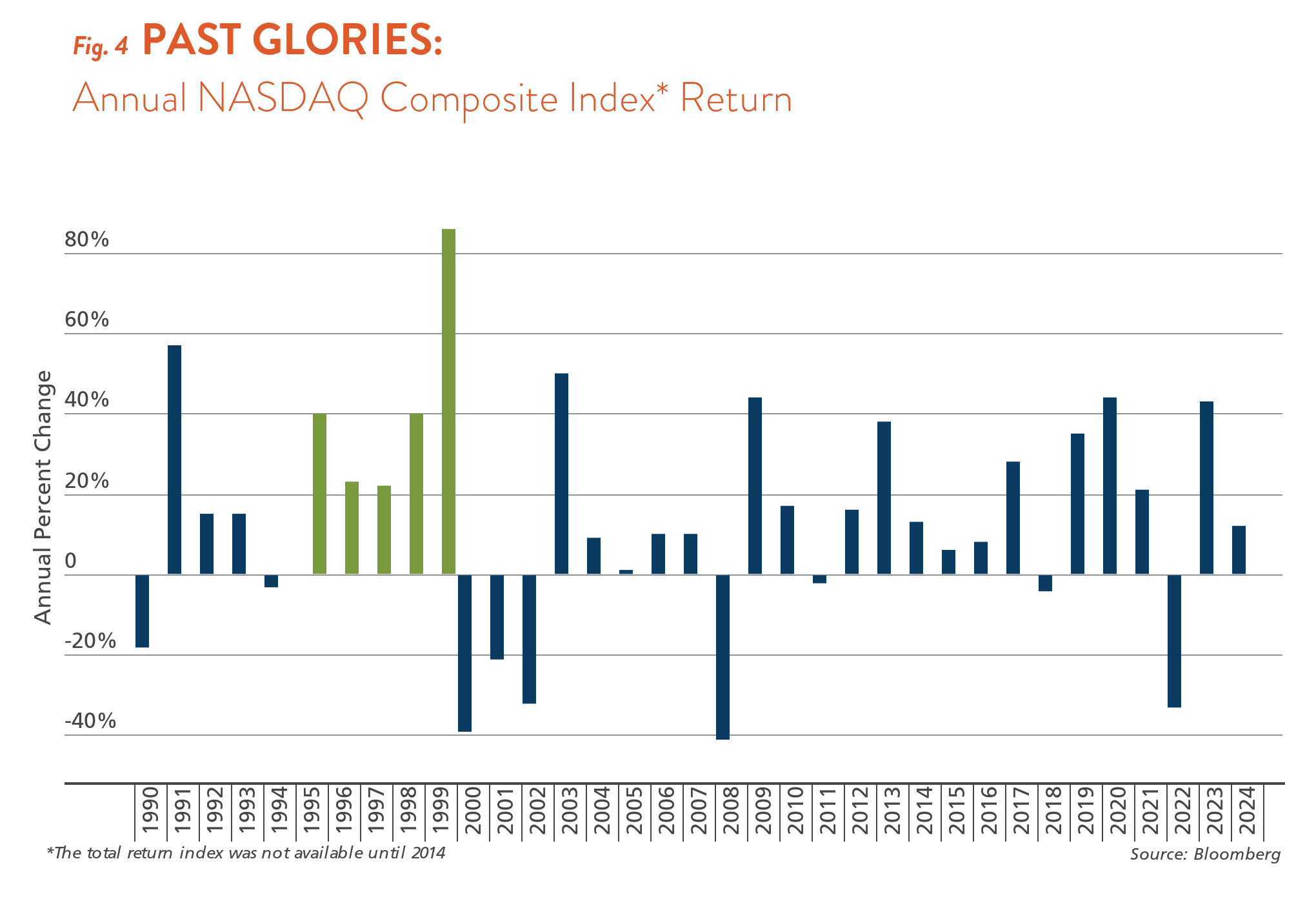

Consequently, the NASDAQ Composite Index increased 789% from January 1990 to December 1999, of which 441% of cumulative gains occurred from 1995 onward, including five consecutive years of 20%+ stock market returns (see Figure 4)—a feat that has not happened since!

As is a typical end to all stories of irrational exuberance, the “dot-com bubble” burst at the turn of the century, leading to the 2001 recession. In Chair Greenspan’s prophetic words, investors might have “underestimated or [become] complacent about the complexity of the interactions of asset markets and the economy.” However, despite its collapse, the 1990s episode featured the birth of the still-dominant tech giants today: Nvidia, Amazon, and Google.

CENTRAL BANK OF THE DECADE

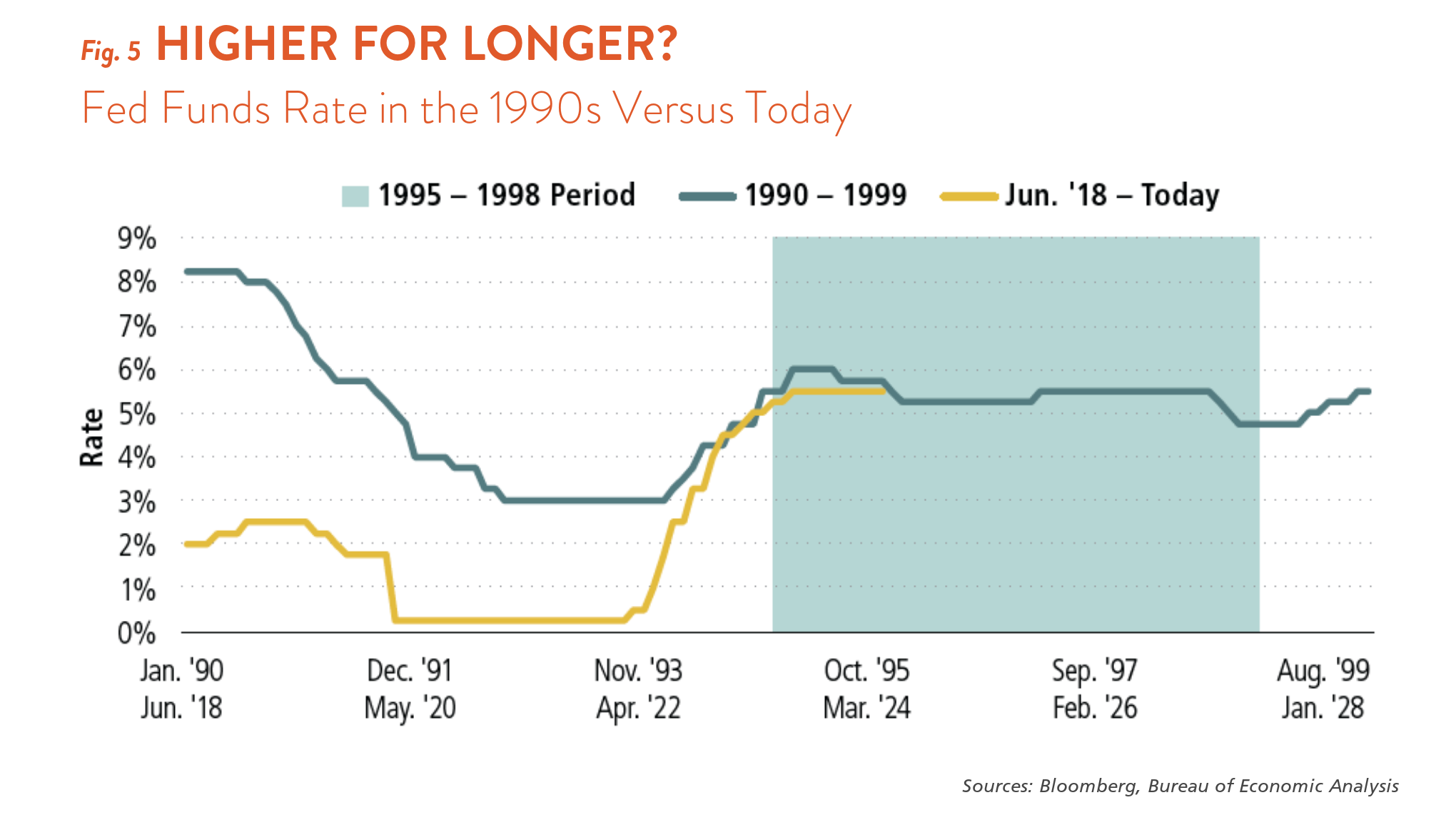

In jest, we say the Federal Reserve earned distinction as the “central bank of the decade” by doing little or nothing for large swaths of the 1990s. The fed funds rate fluctuated in a 100 basis point range from 1995 to 1998 (see Figure 5). But, doing little may have yielded a lot.

Lively debates raged among policymakers as unemployment fell in the mid-1990s. Keynesian thinking promoted the idea that an “overheating” economy would fan inflation. One can forgive policymakers for advancing such a notion, as, having just experienced the 1980s, they thought that only a sharp rise in unemployment squashed inflation so that a reversal would lead to the opposite.

Greenspan won out, though, urging colleagues to consider that the nascent productivity boom would offset price pressures. Greenspan's approach was more of a hunch than a heuristic, as the real-time data did not confirm the theory. Yet Greenspan prevailed over a then-hawkish member of the FOMC, Board Governor Janet Yellen, who pushed for rate hikes.

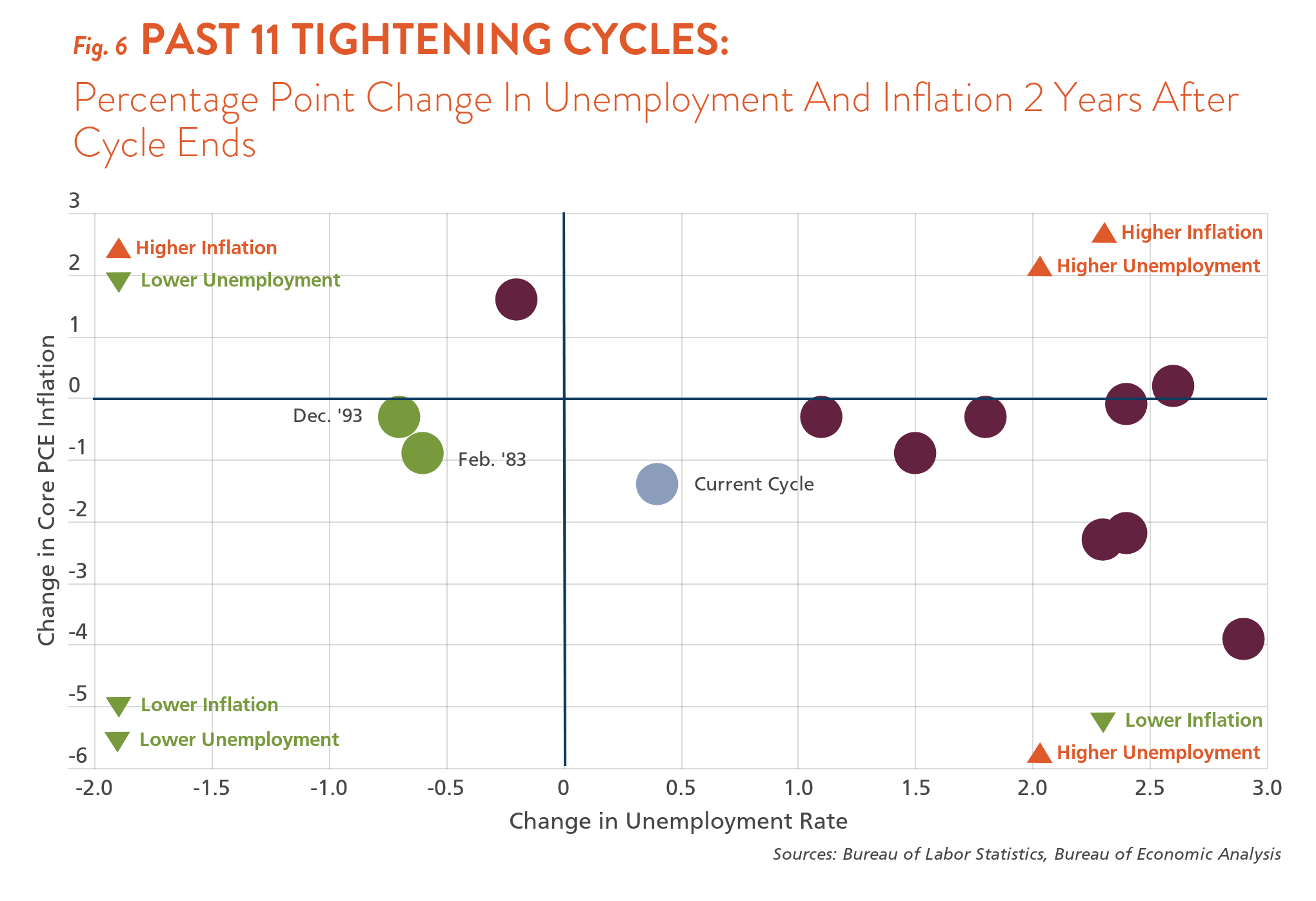

Instead, two years later, the unemployment rate and core PCE inflation were lower than when the Fed started to tighten monetary policy (see Figure 6). Consequently, the 1993–1995 tightening cycle is “the celebrated perfect soft landing that helped make (Chair) Alan Greenspan a central banking legend.”

1990S-STYLE INTEREST RATES

Due to the Fed’s relative inaction and the soft landing that occurred, longer-term interest rates also didn’t move much in the 1990s. For example, the 10-year U.S. Treasury yield traded between 5.50% and 7.00% for 37 months between 1995 and 1998.

Every time the Fed “fine-tuned” (slightly changed) the fed funds rates, the bond market expected something worse for the economy or more aggressive rate cuts. Unfortunately, the Federal Reserve dashed investors’ hopes and fears by either raising rates (1994-1995) or not cutting rates as much as the market anticipated (1995 to 2000).

Younger readers might assume that the Fed’s relative inactivity was due to placid financial markets. But those who lived through it know differently. The early 1990s saw the Resolution Trust Corporation (RTC) wind down hundreds of Savings & Loan organizations (S&Ls), and the bankruptcy of Orange County, California, due to errant interest rate bets.

Also, despite a “laid-back” Fed, in 1997, the Fed stepped in when the Thai baht devalued and contagion spread through Asian financial markets (mainly Thailand, Indonesia, and South Korea). The New York Fed led the U.S. commercial banks with the largest exposure to South Korea in restructuring and extending short-term loans, which helped avoid collective defaults and significant losses on bank balance sheets.7

Similarly, in 1998, with the hedge fund Long-Term Capital Management (LTCM) on the brink after Russia halted its debt payments, the Fed, for the second time, led a joint rescue group of 14 investors who injected capital in exchange for 90% of LTCM’s ownership to prevent the hedge fund from collapsing—a scenario that could have threatened the financial system.8

RECORD PEACE-TIME EXPANSION

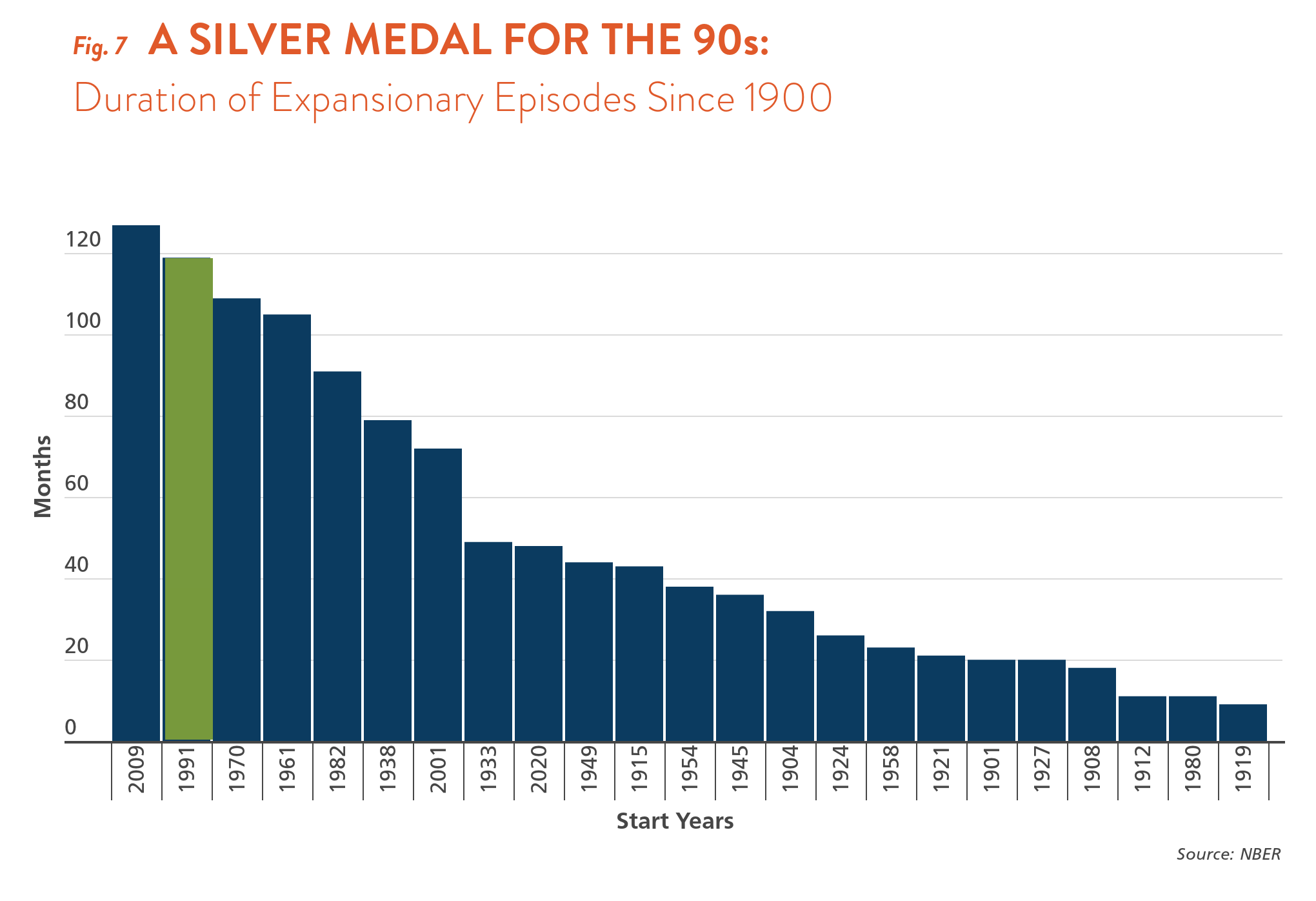

Whoever takes credit—the Fed, Clinton, favorable demographics, a “peace dividend”—by the end of the decade, the economic track record was unequivocal: the 1990s were the best decade of the post-war era (see Figure 7). In an op-ed arguing that the cycle had more room to run, Rudi Dornbusch famously said, “No postwar recovery has died in bed of old age—the Federal Reserve has murdered every one of them.” He concluded his faith in Chair Greenspan's skill, calling him “a great host. He won't remove the refreshments until inflation troubles start. The boom is far from over.”

Despite Greenspan’s misgivings and several financial wobbles, the U.S. economy grew for ten consecutive years (officially: 119 months). Before that, a U.S. recession had occurred every 48 months, on average, in the post-World War II era.

Labor productivity fostered the long peacetime expansion. Productivity averaged 2.7% for the latter half of the decade before averaging just 1.5% from 2005 to 2019. The productivity boom in the 1990s was in plain sight, as the now-San Francisco Fed President Mary Daly recalled, “You could see it everywhere…investments in technology [and] also the tight labor market [were] the forcing function to get businesses moving on [the adaptation of computers].”9

REMAKES ARE NEVER AS GOOD AS THE ORIGINAL

The current decade is still young, so there’s much yet to unfold. But the similarities to the 1990s abound. The decade started with a shock (Covid-19), aggressive central bank tightening (2022-23), financial system worries (SVB), then exuberant financial markets, and the rise of a new generation—the youngest Millennials turned 25 in 2021, with the Millennial cohort projected to reach its peak at 74.9 million in 2033.10 In addition, a nascent productivity boom, led by AI investment instead of dot-coms, is also underway, as 37% of venture capital raised was for software companies (sounds familiar?).11 If growth continues, interest rates may stay elevated.

Admittedly, some pieces are missing, and some new problems exist. Let’s face it: music today is not as good as the 1990s. Also, can India ascend globally to compensate for the lack of another China to enter the international economic fold? Will China dominate global trade (think electric vehicles and electronic appliances)? Relatedly, America’s military might is no longer unrivaled (e.g., China) and seemingly openly challenged (e.g., Russia’s invasion of Ukraine), arguably creating a bipolar world (Beijing versus Washington).

In the end, the remake is never as good as the original. We’ll unlikely see a repeat of the 1990s, and new surprises will surely emerge, but let’s hope we enjoy the balance of the decade as much as we enjoyed the late 1990s, occasional financial wobbles and all.

Please just keep your baggy jeans locked in your closet.

Endnotes

1. Frankel, J. A., & Orszag, P. R. (2002). American economic policy in the 1990s. Page 12. MIT Press.

2. Ibid

3. Fry, R. (2020, April 28). Millennials overtake baby boomers as America’s largest generation. Pew Research Center.https://www.pewresearch.org/short-reads/2020/04/28/millennials-overtake-baby-boomers-as-americas-largest-generation/

4. Federal Reserve Chairman Alan Greenspan’s testimony to Congress in 1987. See Los Angeles Times archives. https://www.latimes.com/archives/la-xpm-1987-09-27-fi-10362-story.html

5. Greenspan, A. (1996, December 5). Remarkes By Chairman Alan Greenspan[Speech transcript]. https://www.federalreserve.gov/boarddocs/speeches/1996/19961205.htm#pagetop

6. National Venture Capital Association. (2011 & 2022). NVCA 2011 Yearbook, NVCA 2022 Year Book. https://nvca.org/nvca-yearbook/

7. Carson, M., & Clark, J. (2013b, November 22). Asian financial crisis. Federal Reserve History. https://www.federalreservehistory.org/essays/asian-financial-crisis

8.Fleming, M., & Liu, W. (2013, November 22). Near failure of long-term capital management. Federal Reserve History. https://www.federalreservehistory.org/essays/ltcm-near-failure

9. Beckworth, D. (Host). (2024, May 13). Mary Daly on Fed Policy, the Economic Impacts of AI, and the Future of the Fed’s Framework. [Audio podcast episode]. Macro Musings. Mercatus Center At George Mason University. https://www.mercatus.org/macro-musings/mary-daly-fed-policy-economic-impacts-ai-and-future-feds-framework

10. Fry, R. (2020, April 28).

11. National Venture Capital Association. (2024). NVCA 2024 Yearbook. https://nvca.org/wp-content/uploads/2024/04/NVCA-2024-Yearbook.pdf