LONG LIVE THE KING: UNDERSTANDING THE ENDURING REIGN OF THE U.S. DOLLAR

In 2023, while one nation crowned a new king (Charles), another king, the U.S. dollar, continued its long reign. With topics like “de-dollarization” gaining mindshare, some investors have expected the dollar to be displaced. But, like it or not, the dollar matters the most, arguably more than ever. We detail four of the top misconceptions dollar bears make.

Bold forecasts that miss the mark are often quickly forgotten or swept under the rug by misfiring prognosticators.

Two years ago, we heard forecasts of “a 30–40% decline in the U.S. dollar.” Even Larry Summers, who correctly anticipated that inflation would become a big problem in the U.S., can’t get full credit for his inflation view—he also predicted a significant drop in the dollar as a critical driver of inflation!1

As everyone now knows, the drop in the dollar didn’t happen. Compared to other developed countries’ currencies, such as the Japanese yen, the dollar is up more than 30% since 2022. Further, since 2011, the dollar is up almost 40% compared to a broad basket of currencies!2 Over the same period, your humble authors have fielded repeated questions about the dollar's inevitable, if not imminent, demise.

So why were the dollar bears so wrong? Popular misconceptions about the dollar's role in the global financial system mislead investors and policymakers alike. Like a monarch’s long reign, these misconceptions never seem to die. We detail our favorite mistakes so that, hopefully, you won’t repeat them.

Scottish philosopher Adam Ferguson wrote that many established institutions are “the result of human action, but not the execution of any human design.”

This quote applies nicely to the institution of the dollar system. Nobody rolled out the blueprints for a global currency system thoughtfully designed from the top down. Instead, the dollar system has more in common with evolutionary biology than architectural design. As economist Perry Mehrling has said, the dollar grew organically.3

For much of its early history, the United States had nothing like a universal currency (see Did You Know? Box: The History of the Dollar). The U.S. followed a bimetallic standard (linked to gold and silver), and paper money was shunned. However, the Panic of 1907 prompted Congress to create the Federal Reserve (Fed).

The history of the dollar predates America’s founding. In 1695, the British banned specie export from England, resulting in perpetual coin shortages in the American colonies. As a result, other commodities (e.g., tobacco and corn) or foreign coins were exchanged. Spanish silver coins were 53 troy grains of silver, or the “real” (royal). The most widely circulated coins were the Spanish silver coins weighing eight royals, or 413.7 grains of silver, and were called “pesos” in English-speaking countries. Pesos became known as “pieces of eight” and “dollars.” The term “dollar” derives from the German word “thaler,” which originated from the Joachimthaler, named after a Bohemian count whose silver coins also circulated widely. The “$” symbol associated with the US dollar today was shorthand for “pesos,” with the “S” representing the plural.18

The Fed later issued “Federal Reserve notes,” lent to banks when liquidity dried up, and enforced “par” settlements for checks across the Federal Reserve System (before that, checks issued by different banks were subject to varying discounts!).

Then came a series of crises and some luck. The U.S.'s favorable geographic location during the First and Second World Wars (far removed from most battlefields) allowed it to become the “center of the global financial system.”4 Owning about 40% of global gold reserves allowed the U.S. to be one of the only countries that did not suspend convertibility throughout the wars.

But hold on a second, you might say, wasn’t the dollar system designed by policymakers at Bretton Woods after the Second World War? In reality, delegates ruled out competing plans as infeasible (see Did You Know? Box: Bancor?). In short, the dollar was just the best and easiest option.

In addition, the dollar’s reign had already gone global. The Euro-dollar market5 was born in the 1920s and was revived in the 1950s because London banks started accepting dollar (and other currencies) deposits and making dollar loans to third parties.6

Did You Know? Bancor?The famous economist John Maynard Keynes pushed a competing plan at Bretton Woods and led the British delegation that proposed a new international settlement asset, the “bancor.” Under the bancor system, a new world central bank would be known as the “Clearing Union.” All countries would have to raise about $30 billion initially to fund the Clearing Union. The total required amount for the Clearing Union would increase to $2.5 trillion 40 years later. No country felt that it was feasible (and perhaps fair?) to supply this sum to the Clearing Union and allow others to have an unlimited usage quota.19 The key to the new reserve currency was stability, which the dollar already had. Keynes later admitted, “There is no longer any need for a new-fangled international monetary unit. Your Lordships will remember how little any of us liked the names proposed—bancor, unitas, dolphin, bezant, daric, and heaven knows what.”20

Finally, when President Nixon “closed the gold window” (severing the link between the dollar and gold) in 1971, it was not some kind of master plan but a temporary fix to deal with the fact that so many dollars lived overseas and fears that foreign dollar holders could demand gold. If anything, slamming the gold window was a threat to the system. Spoiler alert: the dollar teetered but did not topple, and Treasuries replaced gold as the leading reserve asset.7

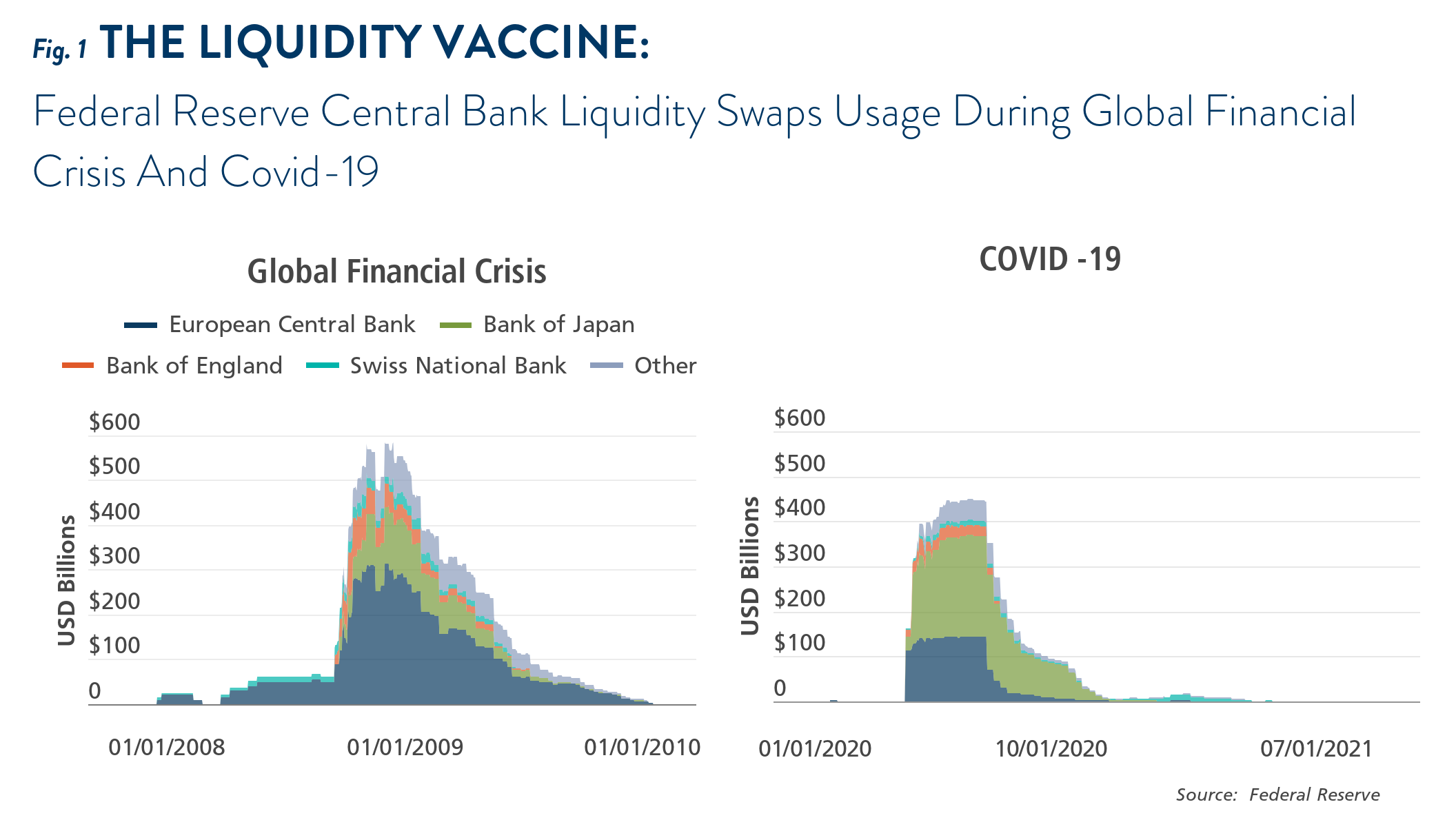

Modern-day crises have only further cemented the dollar’s global reign. During the global financial crisis, the Fed lent $10 trillion in raw swap amounts to its major foreign counterparties, and again during Covid-19—a sign of just how vital the dollar is to the global economy (see Figure 1).8

Today, the global dollar system, although born out of crises, has endured the test of time and proved more resilient and durable than its predecessors.“THE DOLLAR WILL SOON BE DISPLACED BY A RIVAL”Spend time on a trading floor, and you’ll hear references to “currency pairs” or “currency crosses,” such as the EUR/USD. Referring to currencies as pairs or crosses creates the idea that currencies are on equal footing in some sense.

However, currencies are pairs only in the sense mentioned above, as a reference to the exchange rate between two currencies. Indeed, while there are “about 180 currencies in the world, a very small number of dominant currencies play an outsized role in international trade, finance, and central bank foreign exchange reserves.”9

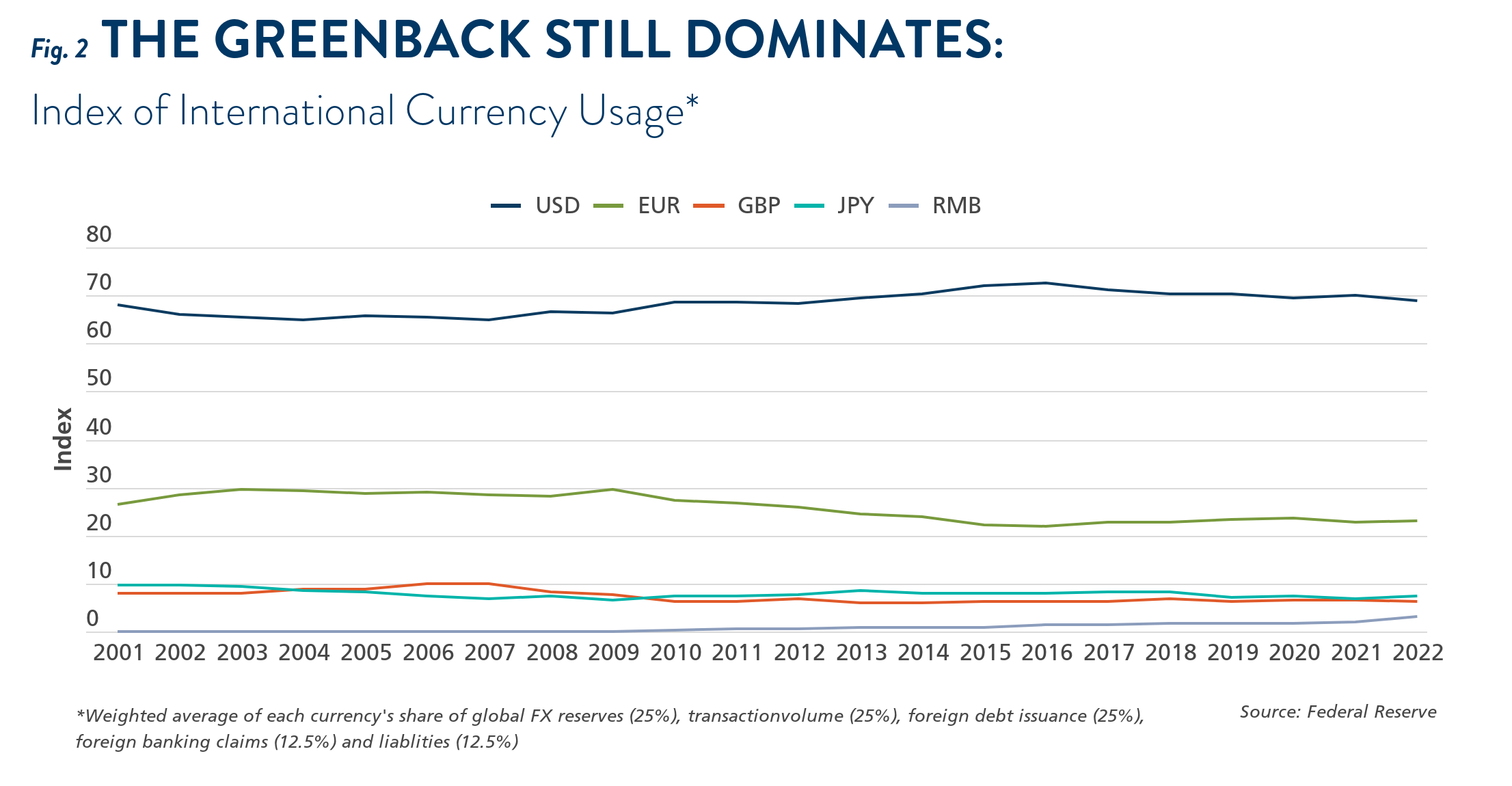

The dollar is the most dominant currency, and its status has waned little in recent decades. According to the international currency index constructed by the Fed, the dollar has remained a steady leader in forex reserves, transaction volume, foreign currency debt issuance, and international banking claims for as long as data is available (see Figure 2).

As for second place? It’s not even close. The euro scores 23 on the index, one-third of the U.S. level, though greater than the sum of the next three currencies combined (Japanese yen (JPY), British pounds (GBP), and Chinese renminbi (RMB)).

The RMB once was the darling of dollar bears, calling for the dollar’s displacement by an ascendant Chinese currency. Since the Chinese stock market crisis in 2015, however, the RMB’s lack of full convertibility, uncertain legal framework, and illiquid financial markets have made it unlikely that it will contend with the dollar’s dominance in the foreseeable future.10

Further, in 2015, countries with currencies anchored to the dollar (not counting the United States) accounted for 50% of world GDP. In contrast, euro-linked economies accounted for just 5% (not counting the euro area).11

In the end, there are no rivals to the dollar’s reign on the horizon.

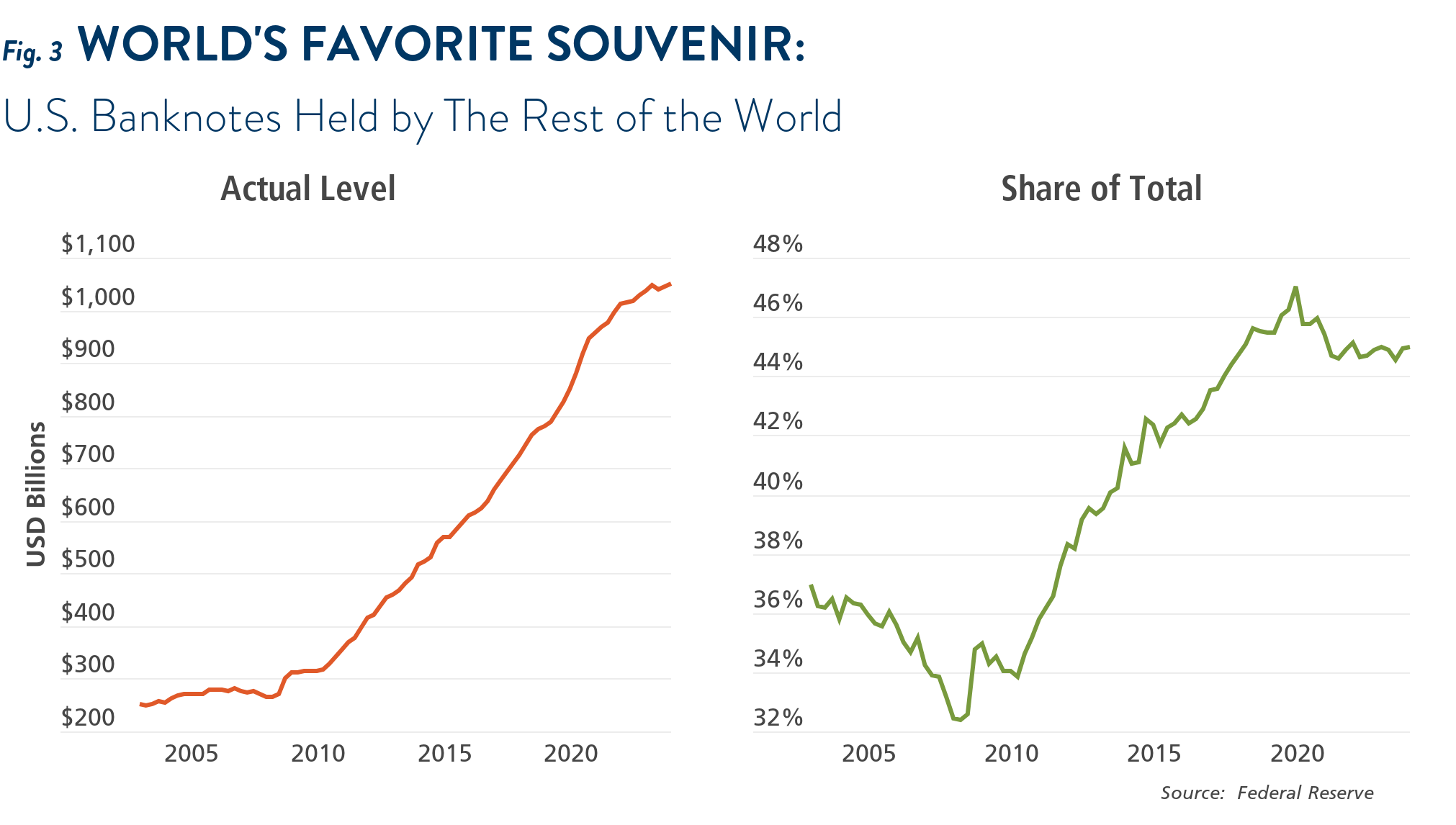

Despite the above facts, the latest dollar bear fad is “de-dollarization.” The argument is that major economies will prefer to use other currencies to avoid the ire of U.S. policymakers keen to “weaponize” the dollar using sanctions.

De-dollarization is catchy and alliterative.

But it’s also wrong (see Figure 3).

First, sanctions are common and have been used for a long time. As early as 1935, the U.S.-led League of Nations (predecessor to the United Nations) sanctioned Italy for its invasion of Ethiopia, banning loans and military equipment.12 In modern times, for military purposes, the U.S. has frozen assets tied to the governments of Libya (2011), Iran (2012), Venezuela (2019), and most recently, Russia (2022).13

Second, the benefits of “dollarization” far outweigh the perceived risk reduction from de-dollarization. Using the dollar allows you to reach 80% of the buyers and sellers in global trade activity (your creditors will invoice you in dollars most of the time!) and the deepest and most liquid financial market in the world.14

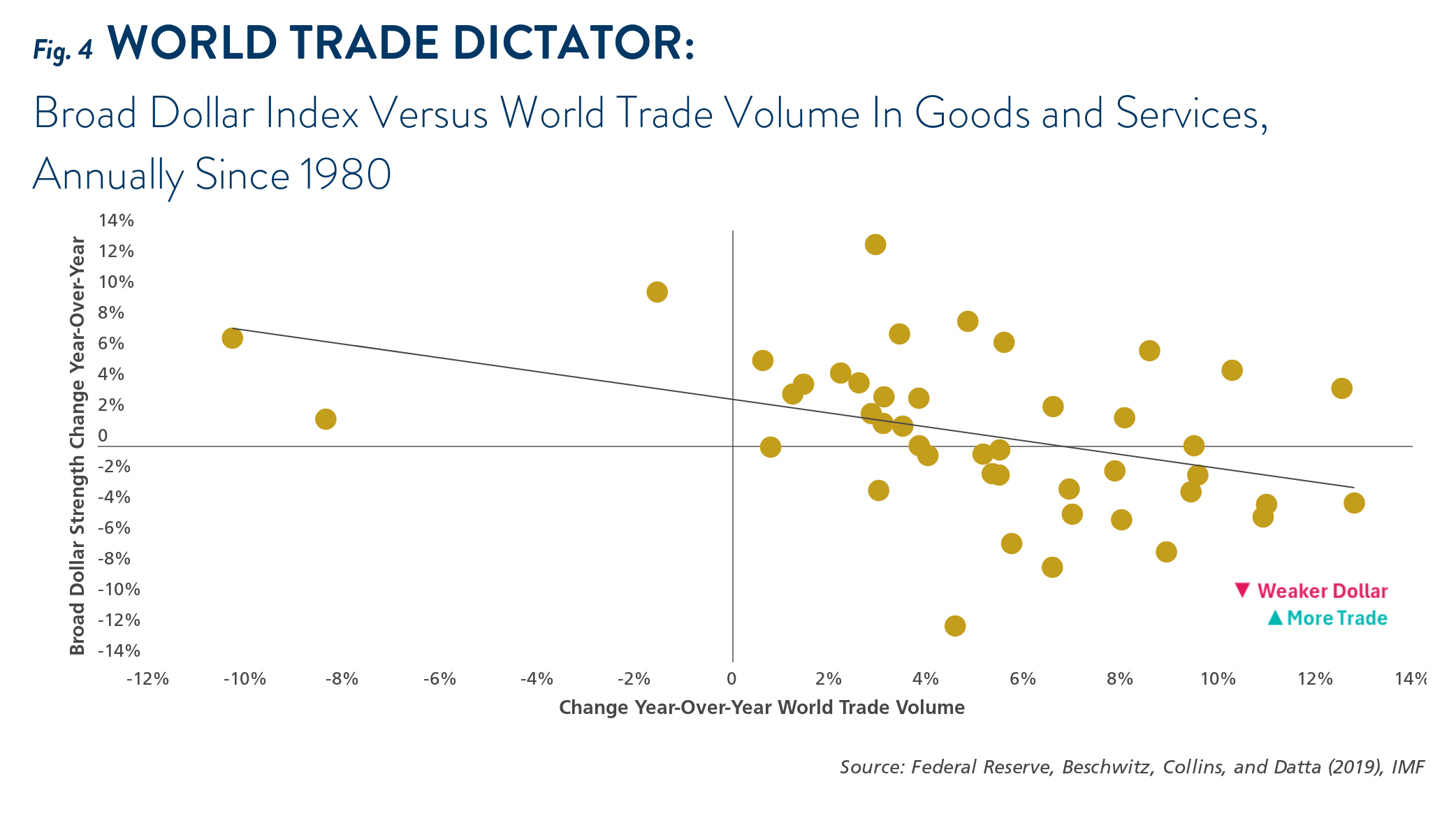

According to a 2023 National Bureau of Economic Research (NBER) research paper, the nominal value of the dollar is directly tied to growth in global economies, especially in developing markets.15 Indeed, a stronger dollar (from higher Fed policy rates or international dollar funding stress) has decreased global asset prices and trade volume in the past (see Figure 4). Trade and capital flows have been primary determinants of growth.

Further, the Fed has proved a reliable backstop for all global financial market participants in past financial crises, notably using central bank swap lines and foreign repurchase agreements. Perhaps it’s better to accept the risk of sanctions associated with the dollar rather than use currencies backed by limited gold reserves or from countries with strict capital controls, who might be reluctant to incur any fiscal deficit.

Finally, one might argue that bad actors ought to be locked out of the dollar financial ecosystem—after all, settling and using dollars is a privilege, not a right. What is the point of having the world’s reserve currency if you cannot use it to further your foreign policy goals?

While instituting sanctions dissuades some countries from holding Treasuries as reserves, it’s unlikely the bulk of dollar reserve holders will dump the dollar. In fact, overseas governments with military ties to the U.S. own nearly three-quarters of the total U.S. debt held by foreign governments.16

In short, the benefits of operating in dollars far outweigh the costs of de-dollarization.

Another common misconception is that the dollar is (always) on the brink of collapse due to excessive debt burden. Headlines often tout the “$27 trillion in marketable debt outstanding.”

From a first approximation, we find this view tedious. For the last 30 years, one could have said the same thing every day of every month in every quarter of every year. So far, the predictive value is nil, for the cumulation of national debt has yet to lead to higher yields or a debt default.

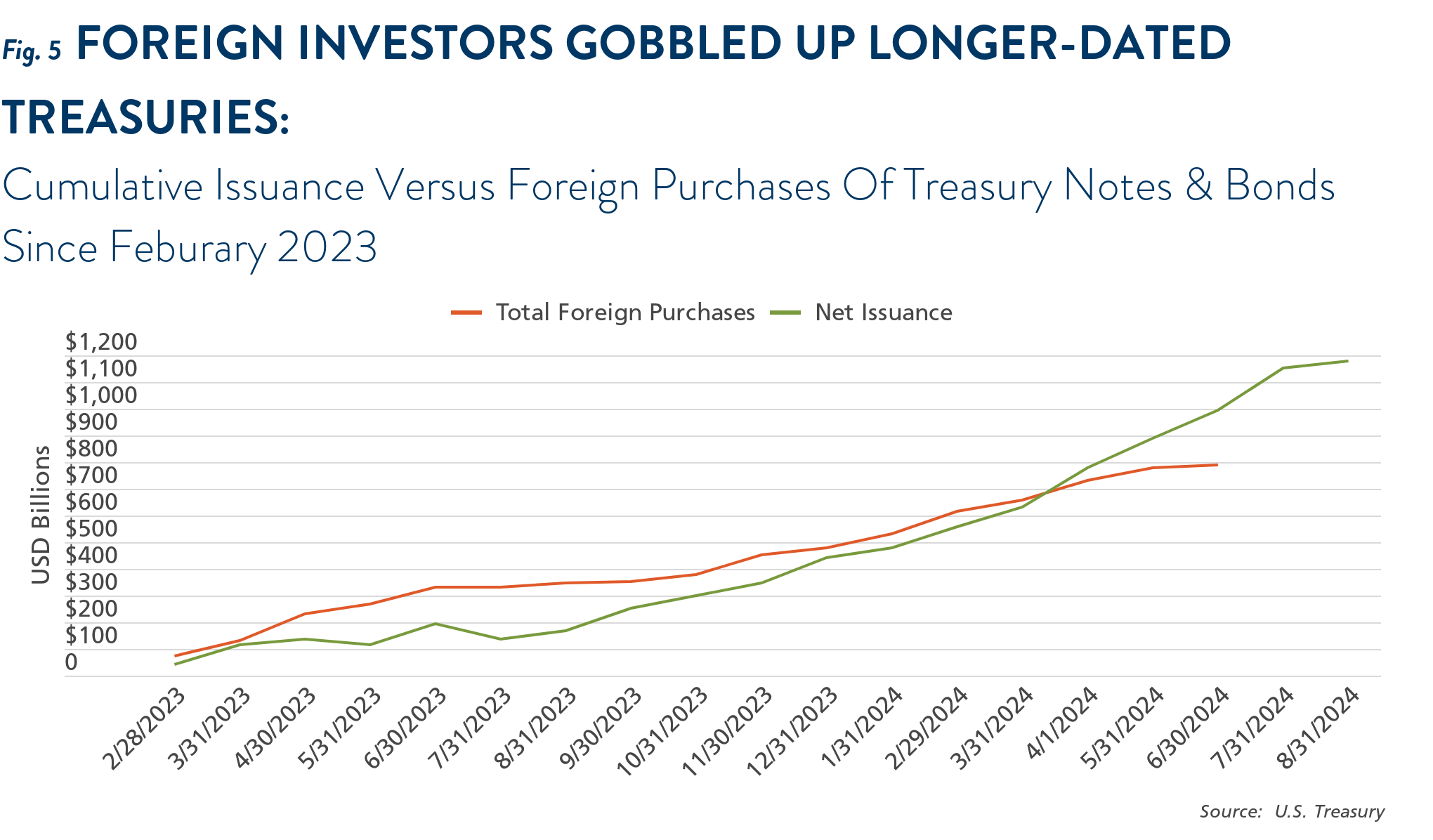

Second, every dollar of debt is not only a liability of the U.S. government but someone else's asset (see Figure 5). And interestingly, it’s a very popular asset, even among foreign investors! Perhaps its popularity is because it is safe (the U.S. has never defaulted) and liquid (with $870 billion in average trades per day in July 2024)17, and offers attractive real returns today (T-bills yield 5.33% versus core inflation of 2–3% in 2024).

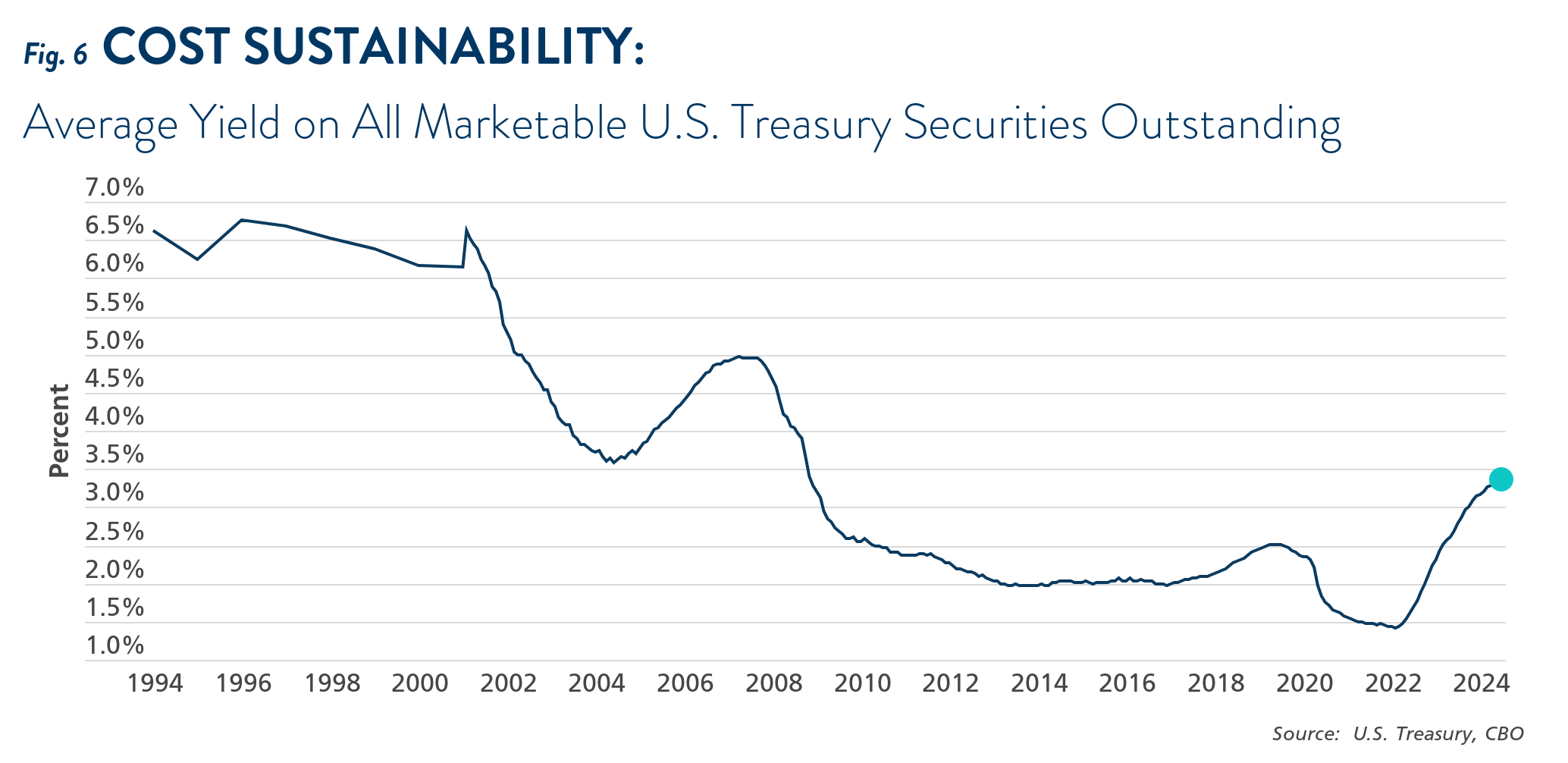

Third, the debt issue is overstated. The average cost (yield) of U.S. debt is only 3.4% as of July 2024, still much lower than most of the country’s recent history, thanks to the dollar's status as the global reserve currency and decades of price stability since the 1990s (see Figure 6). Further, net interest costs, which incorporate the average costs and the total amount of outstanding debt, reached 2.4% of nominal GDP in fiscal year 2023 but are still below its historical high of 3.3%. Unless the fed funds rate stays above 5% for a few more years, we’d argue that the current trajectory of the U.S. debt burden remains manageable.

Dollar doubts stem from four key misconceptions about the dollar system. Rather than a product of design, the dollar is a burgeoning ecosystem that evolved over centuries, proving its resilience and durability. Contrary to popular belief, there are no viable rivals to the dollar. De-dollarization may occur to a limited extent and be led by bad actors in the global financial system. Still, users of the dollar system overwhelmingly benefit from trading, borrowing, and saving in dollars. Further, debt burdens do not yet threaten the dollar system’s stability, with debt service costs manageable and dollar debt buyers more eager than ever to hold greenbacks.

Long live the King?

Endnotes

1. Larry Summers: “We are printing money, we are creating government bonds, we are borrowing on unprecedented scales, those are things that surely create more of a risk of a sharp dollar decline than we had before. And sharp dollar declines are much more likely to translate themselves into inflation than they were historically.” Larry Summers: I Think We're Taking Very Substantial Risks on the Inflation Side | Video | CoinDesk.

2. The Nominal U.S. Broad Dollar Index weights the dollar against a basket of 26 developed and emerging country currencies by trade share with the U.S. For weight details, see https://www.federalreserve.gov/releases/h10/weights/default.htm.

3. Forward Guidance podcast, Dr. Perry Mehrling on The Dollar Standard, Globalization of Shadow Banking, and Charles Kindleberger.

4. Hendrickson, Joshua R., The Treasury Standard: Causes and Consequences (2024, March 14). http://dx.doi.org/10.2139/ssrn.4759755

5. The Euro-dollar market includes all currencies’ deposits and transactions outside its original country. U.S. dollar deposits in London is the center of Euro-dollar market activity.

6. Catherine R. Schenk. (1998, April). “The Origins of the Eurodollar Market in London: 1955-1963.” Explorations In Economic History 35, 221-238.

7. Ibid

8. Tooze, A. (2018). Crashed: How a decade of financial crisis changed the world. (Page 214). Penguin Publishing Group.

9. Itskhoki, O. (2022, March 1). Dominant Currencies. National Bureau of Economic Research. https://www.nber.org/reporter/2022number1/dominant-currencies

10. Amighini, A., & García-Herrero, A. (2023, November 2). Third time lucky? China’s push to internationalise the renminbi. Bruegel. https://www.bruegel.org/policy-brief/third-time-lucky-chinas-push-internationalise-renminbi

11. Weiss, Colin (2022, October). “Geopolitics and the U.S. Dollar’s Future as a Reserve Currency,” International Finance Discussion Papers 1359. Washington: Board of Governors of the Federal Reserve System, https://doi.org/10.17016/IFDP.2022.1359.

12. Coates, B. (2019, December). A Century of Sanctions. Origins. https://origins.osu.edu/article/economic-sanctions-history-trump-global

13. McDowell, Daniel. (2023). Bucking the Buck: U.S. Financial Sanctions & the International Backlash Against the Dollar. Oxford, UK: Oxford University Press.

14. Bertaut, C., Beschwitz, B. von, & Curcuru, S. (2023, June 23). "The International Role of the U.S. Dollar" Post-COVID Edition," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, June 23, 2023, https://doi.org/10.17016/2380-7172.3334.

15. Obstfeld, M., & Zhou, H. (2023, March). The Global Dollar Cycle. National Bureau of Economic Research Working Paper Series, No. 31004. https://doi.org/10.3386/w31004

16. Weiss, Colin (2022).

17. U.S. Treasury Securities Statistics. SIFMA. (2024, August 2). https://www.sifma.org/resources/research/us-treasury-securities-statistics/

18. Nussbaum, A. (1967). A history of the dollar. Columbia U.P.

19. Bernstein, Edward. (1984, May). “Reflections on Bretton Woods.” In The International Monetary System: Forty Years After Bretton Woods, 15-20. Federal Reserve Bank of Boston. https://www.bostonfed.org/-/media/Documents/conference/28/conf28b.pdf

20. Ibid.