NOT ANOTHER AI ARTICLE :

ARTIFICIAL INTELLIGENCE (AI) AS AN INDUSTRIAL PROCESS AND POSSIBLY THE NEXT BIG BUBBLE

While most people encounter artificial intelligence (AI) in the wild as chatbot apps, a massive industrial infrastructure undergirds every query. The buildout in “compute” infrastructure rivals the birth of the Internet Era and may fuel growth in the second half of the 2020s. But will the investment boom also lead to a bust like every bubble before? We explore.

In Greek mythology, Theseus slays the Minotaur in the Labyrinth and escapes using a ball of string he had unspooled on his way in.

In 1952, Bell Labs’ Claude Shannon built Theseus, a little robotic mouse that could navigate around a maze and “learn” the layout to escape using circuit switches. Theseus was the first documented example of machine learning.1

Fast-forward seven decades—and a significant leap forward in computing power—to the debut of ChatGPT in November 2022. The internet has been abuzz with prognostications about artificial intelligence (AI) ever since.

Optimists point to the startling AI capabilities that outperform humans in various tasks. Some think AGI, artificial general intelligence, and then ASI, artificial superintelligence, are right around the corner.

Pessimists point to AI’s embarrassing failures (“hallucinations”) to say the chatbot AI phase is all hype and that a bust will inevitably follow.

We’re suspending judgment, but long-time readers know we're pragmatists. At its heart, AI is an industrial process. Massive investments in hardware, computing, and energy generation are necessary to make AI general intelligence and AI superintelligence possible. Companies continue to scale up to meet current demand for such software and make bold bets on future demand.

Will the frenzy to build out AI boost economic growth throughout the remainder of the decade? And will the huge investment boom eventually lead to a bust, as we witnessed with the original internet buildout?

The primary way in which most of us interact with AI, including ChatGPT, is based on large language models (LLMs). Much like a regression between sales of ice cream and the weather outside, LLMs predict the answer to your question based on your input and as much data as the designer could train the model on.

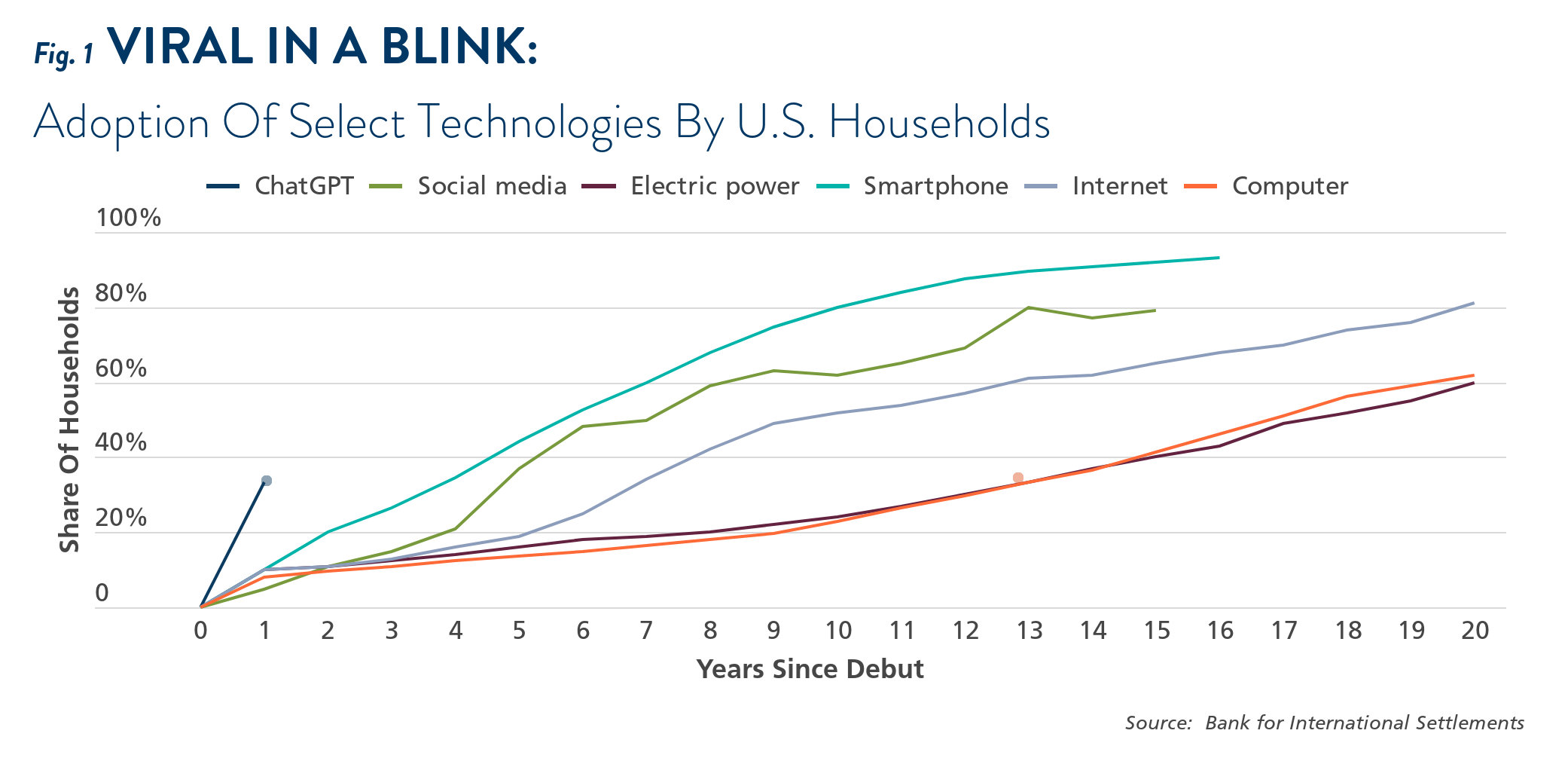

LLMs have turned out to be enormously popular. The first publicly-released version of ChatGPT debuted in November 2022, and it took just a year for a third of U.S. households to try it, a feat that took the personal computer 13 years to achieve (see Figure 1).

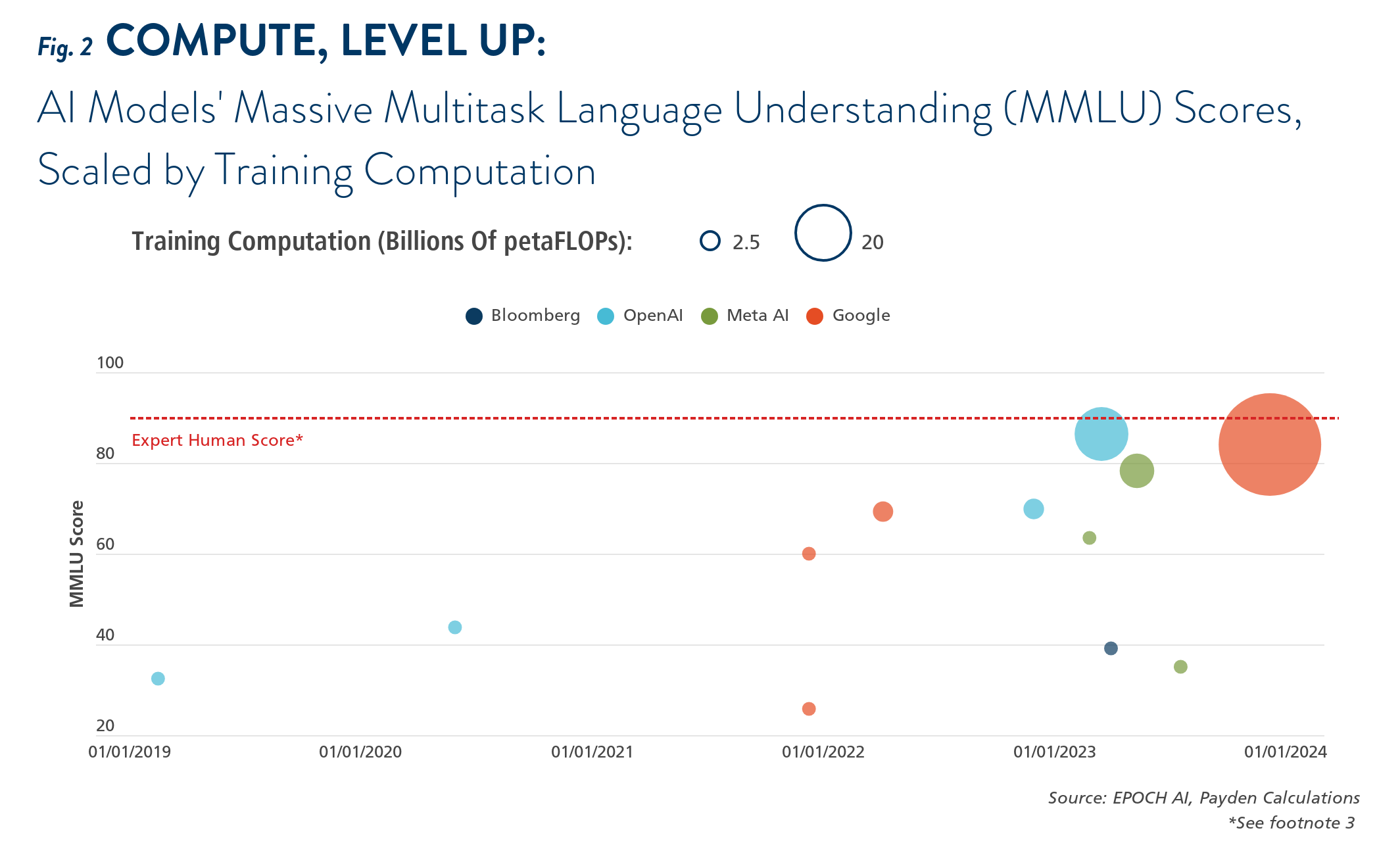

While critics label LLMs as “mere machines” that “autocomplete sentences” with no intelligence, the proof of the pudding is in the eating. They just work. Just a year after GPT-3, ChatGPT improved its model and released GPT-4. Google soon released Gemini Ultra, and Meta released a series of LLaMa models.2 Current models have already started to approach human benchmarks on the Massive Multitask Language Understanding (MMLU) tests, and the latest ones are performing as well as those of human experts (see Figure 2 ).3

What’s responsible for the startling success? Largely, scale. Put enough computing resources behind something, and it can brute-force a helpful result that answers your every ChatGPT query eerily like a human agent.

However, doing so requires massive computing capability. The ChatGPT version released in 2022 required a whopping 21 million petaFLOPs of computing. A petaFLOP is the equivalent of one human adding numbers every second for the next 31,688,765 years.4

Who knows what’s next, but clearly, putting more data and computing resources into LLMs is improving these models—a simple fact that firms and investors have come to realize.

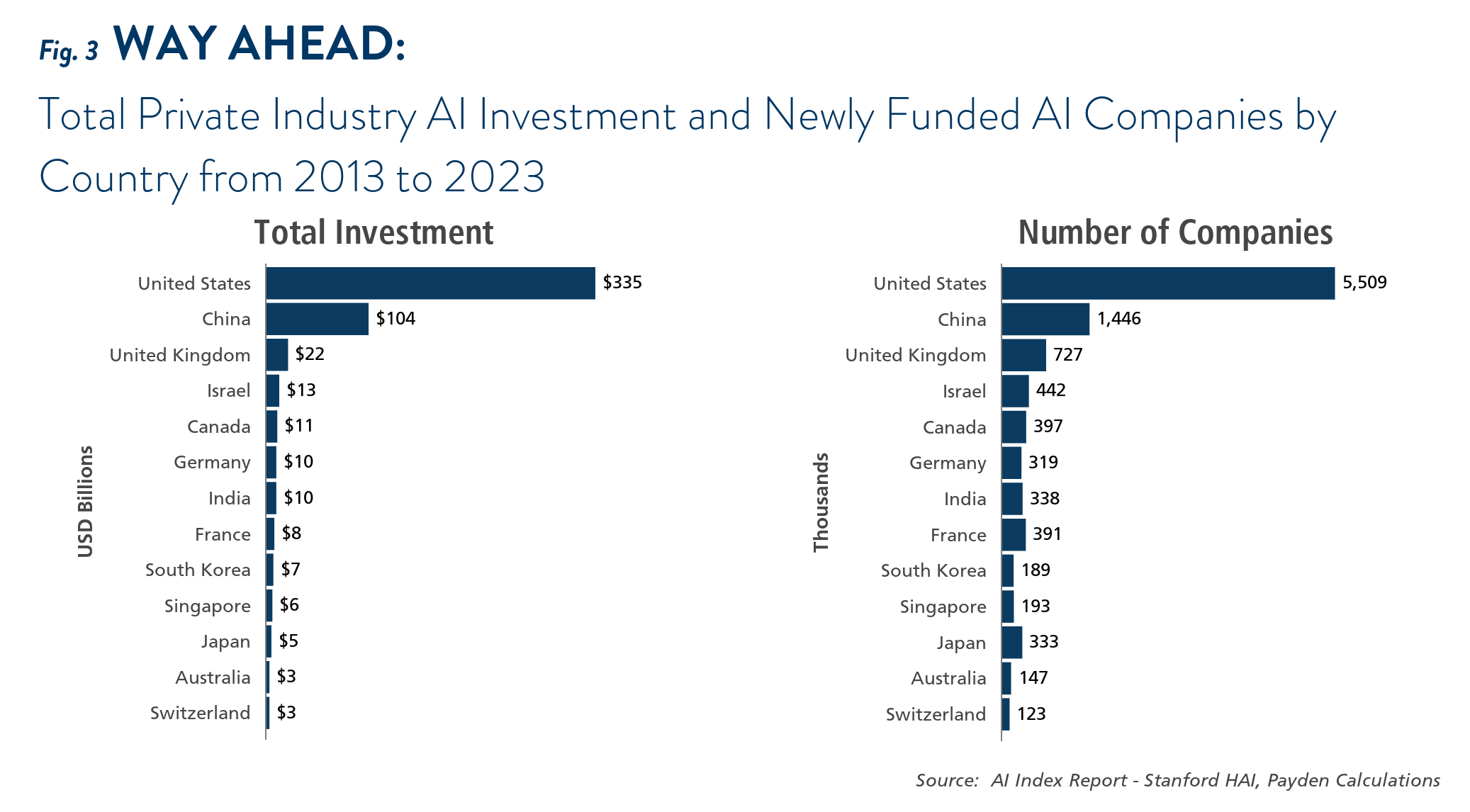

U.S. companies have already spent a whopping $335 billion on AI investment in the last ten years, with 60% of that spent in the previous three years alone.5 For context, the moon landings cost a total of $280 billion between 1960 and 1973 in today’s dollars.6 AI spending has spawned over 5,500 newly funded AI companies (see Figure 3). Put simply, the U.S. private sector is deploying resources at a scale not seen since the days of the Space Race.

What’s more, “hyperscalers”— large tech companies including Meta, Google, Amazon, and Microsoft—are just getting started. Wall Street analysts are expecting more than $213 billion in capital expenditures (capex) on AI in the next three years (enough to build the equivalent capacity to run over 12,000 ChatGPT-4s by 2026).7

In addition, it's not just tech firms rushing to train the best models. The Q1 2024 earnings calls saw 199 companies in the S&P 500 mention “AI,” compared to around 60 companies in 2022!

Capex is required to make models work. AI computing doesn’t float in an imaginary space. Instead, AI lives in data centers, which rely on semiconductors (most commonly GPUs, short for graphic processing units) for processing speed and capacity. Nvidia shipped 3.8 million data center GPUs in 2023—a million more than the year prior.8

Further, total private investment in data center construction increased by $8 billion over 2023 and by another $5 billion in 2024 as of July 2024, which represents a stunning 93% cumulative growth compared to 2022!9 Even with elevated investments, data centers are still in extreme shortage, as the world’s 9,380 data centers still store less than 15% of the total data created in 2023 (see Did You Know? Box: Meet Ashburn, The Data Center Alley).10

As all roads lead to Rome, all investments and growth in AI lead to pent-up electricity (or energy) demand. GPU-filled data centers training AI models require massive electricity usage—on average, one single ChatGPT inquiry uses ten times as much electricity as a Google search.11 Perhaps it’s no surprise that Microsoft—whose data centers run ChatGPT—saw its energy bills at data centers more than double between 2020 and 2023.12

In Ashburn, Northern Virginia, the patch of land near Dulles International Airport hosts about 70% of global internet traffic flow and over 35% of the world’s hyperscale data center capacity.19 How, you wonder, did Ashburn become the national (and perhaps international) hub for data centers? First, connectivity matters. Ashburn enjoys the highest density of fiber optics in the world (some from experiments starting in the 1960s).20 In addition, cheap commercial electricity and an abundance of water for cooling are friendly environments for data centers. Lastly, there are network effects. Upon the first data center being established in the 1990s, data centers subsequently clustered in Ashburn, as proximity to other data centers allowed for easy “backup.” However, despite Ashburn’s dominance, the momentum of data center construction has just begun: data center vacancies dropped from 10% in 2018 to a record 3.7% as of Q1 2023, and Ashburn data center rents increased 46% in 2023.21 As data centers expand their geographical diversity and coverage, Ashburn’s story could be the key to success.

With the AI-style space race in focus for all types of firms, data center power demand is expected to increase by 160% and be nearly one-tenth of world energy consumption by 2030, up from today’s 1%. Generating enough energy to feed the AI machine may require new energy sources (including leading renewables and nuclear) and newer power grids to meet the rising demand. In short, AI demand may spark another energy revolution.

Scientist and historian Jared Diamond wrote, “Technology finds most of its uses after it has been invented, rather than being invented to meet a foreseen need.”13

Indeed, one can characterize the internet buildout—specifically the rise and fall of telecommunications in the 1990s—as a technological invention that drove investment into the internet, just maybe a little too early and fast.

Investment in telecom, or connectivity infrastructure (such as optical fibers), is one of the largest bases of capital ever built in such a short time. Investment in information processing equipment and software grew at an average quarterly annualized rate of 21% between 1995 and 1999.14

Much like semiconductors and data centers are backbones of AI, telecommunication equipment and computer hardware are the picks and shovels of the internet. At the peak, the telecom capex was approximately $120 billion ($224 billion in today’s dollars), with cumulative investments worth over $1 trillion in today’s dollars.15

However, overinvestment led to the financial market pullback and a mild recession in the early 2000s. When the telecom bubble burst, less than 3% of fiber laid out in large cities in the U.S. carried any signals, and only 10% of the available global wavelengths were operational.16 Suddenly, the price of fiber collapsed, as did computers, which experienced an average annual decline of 21% in prices from 1995 to 2000. The price of the semiconductors that went into those computers also decreased by nearly 50% on average during the same period.17

But the story didn’t end there. Surplus capacity lowered costs in the long run. The abundance of fiber infrastructure and cheap computers became the bedrock for the rise of new industries, including smartphones (the iPhone in 2007), video streaming (YouTube in 2005 and Netflix in 2007), social media (Facebook in 2004), and cloud computing (Amazon and Google launched web services in 2006). Firms were more eager than ever to pay for higher-speed internet and faster computers, especially companies in the financial industry, which relied on transaction speed and efficiency for competitive advantage.

It took almost ten years from the signing of the Telecommunications Act of 1996 to see internet traffic running through unused fibers on the ground and ocean floor again. By 2011, the nation was again laying 19.2 million miles of fiber to accommodate growing demand—a pace mirroring those at the peak of the telecom bubble.18

In the same vein, an AI bust may be inevitable in the short term.

Like the telecom crash, the bust would purge speculative ventures and unsustainable business models. However, lasting infrastructure, from advanced semiconductors to vast data centers, and intellectual advancements, from aerospace inventions to another energy revolution, could pave the way for the next wave of innovation.

Additionally, the workforce trained during this period—data scientists, AI engineers, and software developers—will have the skills to innovate in ways we can’t envision today. Even if investor enthusiasm cools, AI's practical applications will continue transforming many fields, whether it is through long-term productivity gains or new market opportunities.

Ultimately, we don’t know when or whether AI will deliver on the ambitious promises investors imagine today. What we suspect, though, is that, like the telecom boom and bust, AI will leave a transformative legacy in ways we may never expect.

Endnotes

1. Klein, D. (2024, August 22). Mighty Mouse. MIT Technology Review. https://www.technologyreview.com/2018/12/19/138508/mighty-mouse/

2. LLaMA is short for large language model Meta AI.

3. Massive Multitask Language Understanding (MMLU) test includes 57 multiple choice questions that cover math, physics, history, computer science, law, professional medicine, and others. A human benchmark is extrapolated by taking the accuracy of the 95th percentile human on exams. See Hendrycks et. al. (2021, January). Measuring Massive Multitask Language Understanding. https://arxiv.org/pdf/2009.03300

4. Indiana University. (2023, May 5). Understand Measures of Supercomputer Performance and Storage System Capacity. Indiana University Knowledge Base. https://kb.iu.edu/d/apeq

5. R. Perrault, J. Clark et. all. (2024, April). The AI Index 2024 Annual Report. AI Index Steering Committee, Institute for Human-Centered AI, Stanford University. https://aiindex.stanford.edu/wp-content/uploads/2024/05/HAI_AI-Index-Report-2024.pdf

6. Dreier, C. (2022). An Improved Cost Analysis of the Apollo Program. Space Policy, 60, 101476. https://doi.org/10.1016/j.spacepol.2022.101476

7. Barclays Research Estimates assumes ChatGPT uses about 200 million DAU (daily active users) and average user queries per DAU of 1.25 for image and text. For more details, see R. Sandler, T. Young, T. Long, T. O’Malley. (2024, June 25). Cloud AI Capex: FOMO or Field-Of-Dreams? Barclays Research.

8. Shah, A. (2024, June 11). Nvidia Shipped 3.76 Million Data-center GPUs in 2023, According to Study. HPCwire.

9. U.S. Census Bureau. (2024, July). Construction Spending Historical Value Put in Place, Monthly. https://www.census.gov/construction/c30/historical_data.html

10. Laughlin, M., & Footh, J. (2024, February 22). Data Center Growth Abounds in the Digital Age. PGIM Real Estate. https://www.pgim.com/real-estate/commentary/data-center-growth-abounds-digital-age

11. AI is poised to drive 160% increase in data center power demand. Goldman Sachs. (2024, May 14). https://www.goldmansachs.com/insights/articles/AI-poised-to-drive-160-increase-in-power-demand

12. 2024 Environmental Sustainability Report. Microsoft. https://query.prod.cms.rt.microsoft.com/cms/api/am/binary/RW1lMjE

13. Diamond, J. M. (2017). Guns, Germs, and Steel: The Fates of Human Societies. Norton.

14. U.S. Bureau of Economic Analysis. Gross Domestic Product. Assessed 2024, September.

15. Ibid.

16. Hecht, J. (2016, October). Boom, Bubble, Bust: The Fiber Optic Mania. Optics & Photonics News, Quantum Computing: How Close Are We?. Retrieved from https://internethistory.org/wp-content/uploads/2020/01/OSA_Boom.Bubble.Bust_Fiber.Optic_.Mania_.pdf; Dreazen, Y. J. (2002, September 26). Wildly Optimistic Data Drove Telecoms to Build Fiber Glut. The Wall Street Journal. https://www.wsj.com/articles/SB1032982764442483713

17. M. Doms. (2004). The Boom and Bust in Information Technology Investment. FRBSF Economic Review 2004. Federal Reserve Bank of San Francisco. https://www.frbsf.org/economic-research/wp-content/uploads/sites/4/er19-34bk.pdf

18. Troianovski, A. (2012, April 3). Optical delusion? fiber booms again, despite bust. The Wall Street Journal. https://www.wsj.com/articles/SB10001424052702303863404577285260615058538

19. W. Thompson, H. Greenberg, S. Gupta, N. Campanella, T. Long, B. Lynch, T. O’Malley, S. Fessler.(2024, June 27). Powering AI: Calibrating US Data Center Energy Demand. Barclays Research.

20. The Dawn of Data. Virginia Economic Development Partnership. (2019). https://www.vedp.org/news/dawn-data.

21. CBRE. (2024, March 6). North America Data Center Trends H2 2023. https://www.cbre.com/insights/reports/north-america-data-center-trends-h2-2023.